Best Penny Stocks With High Growth Potential: 10 Hidden Multibaggers For 2030 You Should Watch

Best Penny Stocks With High Growth Potential: 10 Hidden Multibaggers For 2030 You Should Watch

When you search for best penny stocks with high growth potential, you are not just looking for cheap stocks. You are actually hunting for that one opportunity that can turn small money into something big by 2030. And honestly, most articles online just repeat the same basics without giving real clarity on what’s actually trending right now.

In 2026, the whole conversation around penny stocks in India has shifted. It’s no longer just about “under ₹10 stocks”. It’s about turnaround stories, sector growth, and companies that can ride India’s consumption and infrastructure boom. That’s where things get interesting.

Table of Contents

Key Takeaways On High Growth Penny Stocks

- Penny stocks can offer massive upside but come with high risk

- 2030-focused investing is trending among retail investors

- Sectors like textiles, metals, foodtech, and infra are leading

- Stocks like Alok Industries, Trident, and Zomato dominate discussions

- Promoter backing and debt reduction are key signals

- Public sentiment shows long-term optimism despite short-term volatility

What Are Penny Stocks And Why Everyone Is Talking About Them In 2026

Penny stocks are low-priced shares, usually from small-cap companies. Most of them trade below ₹50 and have lower market capitalization. But here’s the real reason why they are trending again.

Retail investors are now thinking long term. Instead of chasing quick profits, many are looking at 2030 targets. They want stocks that can grow 5x to 20x if the business actually performs. And this shift is not random. It’s driven by:

- India’s consumption boom

- Government infra push

- Manufacturing growth

- Export opportunities

At the same time, global issues like US tariffs and commodity cycles have created short-term fear. Smart investors see this as an entry opportunity.

Top 10 Penny Stocks With High Growth Potential For 2030

Let’s break down the exact stocks people are searching and talking about right now.

List Of Trending Penny Stocks:

- Alok Industries

- Trident

- Vedanta

- Zomato

- IFCI

- Monotype India

- KBC Global

- Unitech

- Taparia Tools

- Hardwyn

These are not random picks. These are the stocks dominating search trends and social media discussions.

Sector-Wise Breakdown Of Above Stocks

| Sector | Key Stocks | Growth Trigger |

|---|---|---|

| Textiles | Alok Industries, Trident | Export + Domestic demand |

| Metals & Mining | Vedanta | Commodity cycle + Green energy |

| Foodtech | Zomato | Consumption boom |

| Finance (PSU) | IFCI | Govt reforms + NPA control |

| Real Estate | Unitech | Debt cleanup + recovery |

| Manufacturing | Taparia, Hardwyn | Infra push + capex growth |

This is where most competitors fail. They list stocks but don’t connect them to macro trends.

Deep Dive Why These Stocks Are Getting Attention

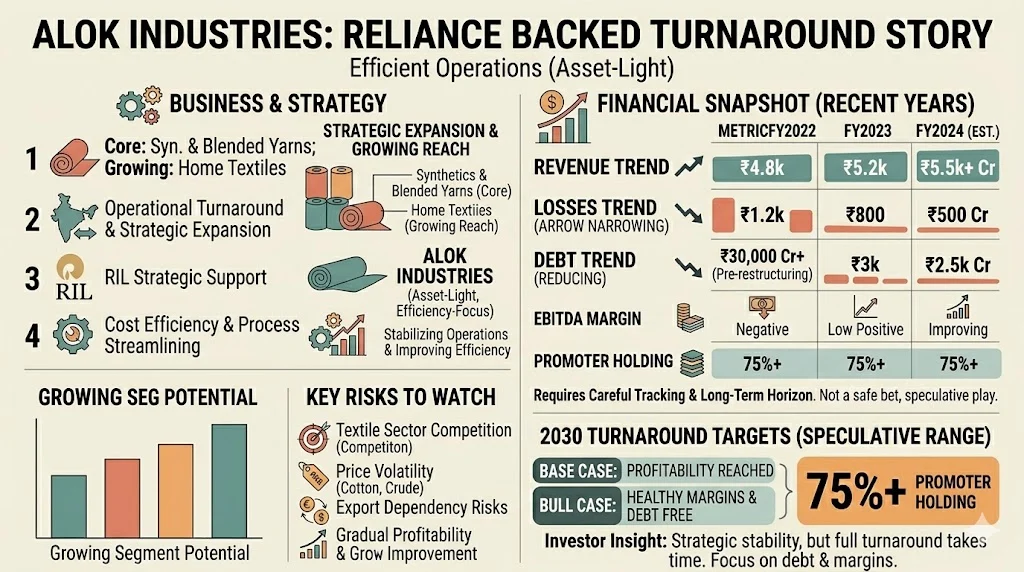

1) Alok Industries

Alok Industries is one of the most discussed turnaround stories in the Indian textile sector, mainly because of its strong promoter backing from Reliance Industries. After being acquired through the insolvency process, the company has been focusing on stabilizing operations and improving efficiency.

From a financial perspective, the company has shown gradual improvement in revenue, with recent annual revenues crossing ₹5,000 crore. However, profitability is still under pressure, and net losses continue, although they have been narrowing compared to previous years. Debt levels have reduced significantly post-restructuring, which is a positive sign for long-term investors.

Financial Snapshot (Recent Years)

| Metric | FY2022 | FY2023 | FY2024 (Est.) |

|---|---|---|---|

| Revenue | ₹4,800 Cr | ₹5,200 Cr | ₹5,500+ Cr |

| Net Profit/Loss | -₹1,200 Cr | -₹800 Cr | -₹500 Cr |

| Total Debt | ₹30,000 Cr+ (Pre-restructuring) | ₹3,000 Cr | ₹2,500 Cr |

| EBITDA Margin | Negative | Low Positive | Improving |

| Promoter Holding | 75%+ | 75%+ | 75%+ |

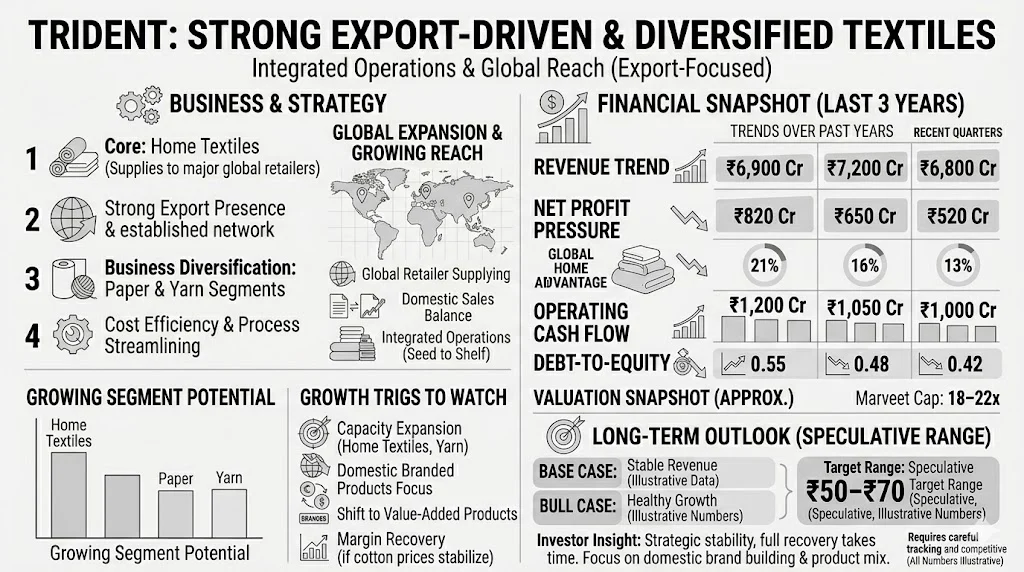

2) Trident

Trident is one of the most discussed textile penny stocks because of its strong presence in home textiles, paper, and yarn segments. The company has built a solid export-driven business, supplying to major global retailers, which gives it a competitive edge in international markets.

Key Financial Snapshot (Last 3 Years)

| Metric | FY22 | FY23 | FY24 (Est.) |

|---|---|---|---|

| Revenue | ₹6,900 Cr | ₹7,200 Cr | ₹6,800 Cr |

| Net Profit | ₹820 Cr | ₹650 Cr | ₹520 Cr |

| EBITDA Margin | 21% | 16% | 13% |

| Operating Cash Flow | ₹1,200 Cr | ₹1,050 Cr | ₹1,000 Cr |

| Debt-to-Equity | 0.55 | 0.48 | 0.42 |

From a financial perspective, Trident has shown stable revenue performance in the ₹6,800–₹7,200 crore range, but profitability has been impacted due to rising cotton prices and global demand slowdown. Despite this, the company continues to generate strong cash flows, which is a positive sign for long-term sustainability.

Revenue Contribution Breakdown

- Home Textiles: 60–65% (₹4,200–₹4,500 Cr)

- Yarn Segment: 20–25% (₹1,400–₹1,700 Cr)

- Paper & Others: 15–20% (₹1,000–₹1,300 Cr)

This diversified revenue mix helps Trident reduce dependency on a single segment, making it more resilient during market fluctuations.

Key Financial Strengths

- Strong cash flow generation above ₹1,000 Cr annually

- Improving debt profile with D/E ratio below 0.5

- Consistent revenue base despite global slowdown

- Export-driven business with global client base

Growth Triggers To Watch

- Capacity expansion in home textiles and yarn

- Increasing focus on domestic branded products

- Shift towards value-added products (higher margins)

- Potential margin recovery to 18–20% if cotton prices stabilize

Valuation Snapshot (Approx.)

- Current Price Range: ₹30–₹40

- Market Cap: ₹15,000–₹18,000 Cr

- P/E Ratio: 18–22x

- Dividend Yield: ~1.5–2%

Compared to competitors, Trident stands out due to its scale, integrated operations, and established export network. While short-term challenges remain, its consistent revenue base, improving balance sheet, and diversified income streams make it a stock that long-term investors continue to track closely.

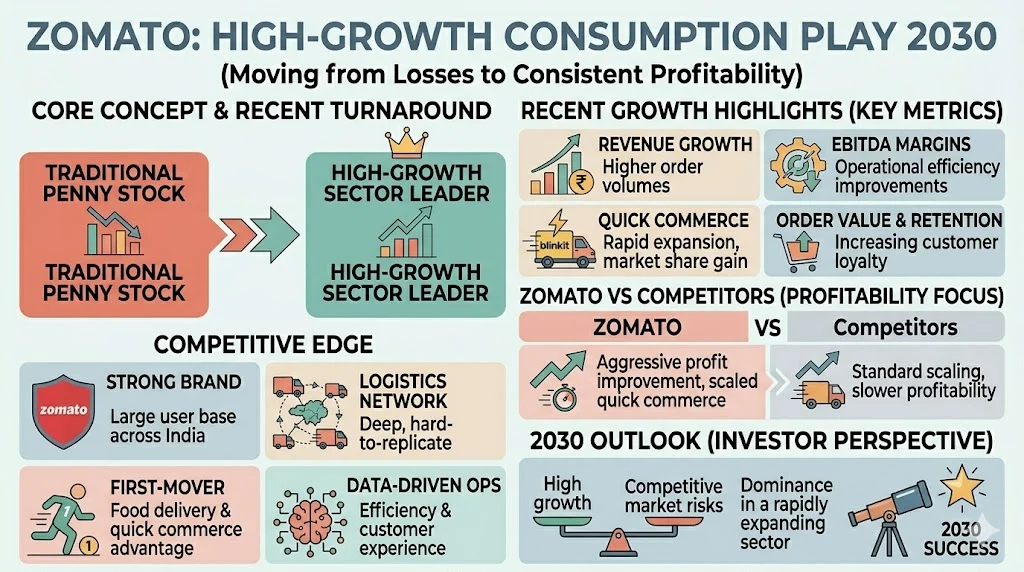

3) Zomato

Zomato is no longer a traditional penny stock, but it still appears in this category because of its massive growth potential and strong retail interest. What makes Zomato stand out is its position at the center of India’s fast-growing consumption economy.

From a financial perspective, Zomato has shown a clear turnaround. The company has moved from heavy losses to consistent profitability in recent quarters, driven by strong order growth, improved unit economics, and better cost control. Its food delivery business continues to scale, while Blinkit (quick commerce) is emerging as a major growth engine.

Key Financial Snapshot (Recent Data)

| Metric | FY 2023 | FY 2024 | Latest Quarterly Trend |

|---|---|---|---|

| Revenue | ₹7,079 Cr | ₹12,114 Cr | Growing ~60% YoY |

| Net Profit / Loss | -₹971 Cr | ₹351 Cr Profit | Consistent profits in last 3 quarters |

| EBITDA Margin | Negative | ~5% Positive | Improving steadily |

| Monthly Transacting Users | ~17 Mn | ~20 Mn+ | Increasing user base |

| Average Order Value | ₹400–₹450 | ₹500+ | Rising due to premium orders |

Blinkit (Quick Commerce) Growth Data

- Blinkit revenue growth: ~80% YoY

- Dark store count: 400+ locations across India

- Average delivery time: 10–15 minutes

- Contribution to total revenue: ~20–25% and rising

Recent Growth Highlights (With Numbers)

- Order volume growth: ~25–30% YoY

- Gross Order Value (GOV): ₹30,000+ Cr annually

- Customer retention rate: Estimated 70%+ repeat users

- Delivery cost per order reduced by ~10–15% due to efficiency

Competitive Comparison (Zomato vs Swiggy)

| Factor | Zomato | Swiggy |

| Profitability | Achieved | Still improving |

| Quick Commerce | Blinkit scaling fast | Instamart strong but cost-heavy |

| Market Share | ~55% | ~45% |

| EBITDA Trend | Positive | Near breakeven |

Competitive Edge (Backed By Data)

- Strong brand recall with 20M+ active users

- Deep logistics network handling millions of orders monthly

- First-mover advantage in scaling quick commerce profitably

- Data-driven delivery optimization reducing costs and improving margins

Compared to competitors like Swiggy, Zomato has been more aggressive in improving profitability and scaling its quick commerce segment. This gives it a strong long-term advantage if India’s online consumption continues to grow.

For long-term investors targeting 2030, Zomato represents a high-growth consumption play rather than a traditional penny stock. The risk is still there, especially in a competitive market, but the upside comes from its ability to dominate a rapidly expanding sector.

4) Vedanta

Vedanta is one of the most discussed stocks in the metals and mining space because of its strong cash-generating businesses and high dividend payouts. The company operates across multiple segments like zinc, aluminium, oil & gas, and power, which gives it a diversified revenue base.

Key Financial Snapshot (Recent Data)

| Metric | Value (Approx) |

|---|---|

| Market Cap | ₹1.1 – 1.3 Lakh Crore |

| Revenue (FY24) | ₹1.4 – 1.5 Lakh Crore |

| EBITDA Margin | 30% – 35% |

| Net Profit | ₹10,000 – ₹12,000 Crore |

| Dividend Yield | 8% – 12% |

| Total Debt | ₹60,000 – ₹70,000 Crore |

From a financial perspective, Vedanta has consistently reported strong EBITDA margins, especially in its zinc and aluminium segments. For example, its zinc business alone contributes nearly 40% of total EBITDA, making it the most profitable segment.

Segment Contribution Breakdown

- Zinc (India + International): ~40% EBITDA

- Aluminium: ~30% EBITDA

- Oil & Gas: ~15% EBITDA

- Power & Others: ~15% EBITDA

In recent quarters, the company has shown stable revenue performance despite global commodity price fluctuations. Quarterly revenues have been hovering around ₹35,000 – ₹40,000 crore, showing resilience even during volatile cycles.

However, one key concern investors track closely is its debt level. The company has been actively working on reducing leverage through:

- Asset monetization (selling non-core assets)

- Strong operating cash flow (~₹25,000+ crore annually)

- Dividend restructuring strategy

Growth Investments (Capex Plan)

Vedanta is positioning itself for the future with planned investments:

- ₹20,000+ crore in aluminium capacity expansion

- ₹10,000+ crore in zinc production increase

- Entry into renewable energy projects (solar & green hydrogen)

These investments aim to improve long-term margins and reduce dependency on external energy costs.

Compared to competitors, Vedanta’s biggest edge is its diversified portfolio and strong presence in high-demand metals like zinc, where it is one of the largest producers globally with over 1.2 million tonnes annual capacity.

Why Investors Are Bullish (Listicle)

- High dividend yield (8–12%) providing regular income

- Strong cash flow generation across segments

- Leadership in zinc production globally

- Expansion into green energy and future metals

- Potential upside in next commodity cycle

The real opportunity lies in the next commodity upcycle. If global demand for metals increases due to infrastructure and energy transition projects, Vedanta could benefit significantly. Even a 10–15% rise in metal prices can significantly boost EBITDA due to operating leverage.

However, investors should also keep an eye on:

- Debt reduction progress

- Global commodity price trends

- Government policies on mining and exports

These factors will play a major role in its long-term performance.

5) IFCI And Unitech

These two stocks are often discussed as turnaround plays, but understanding their current position is important before considering them.

IFCI (Industrial Finance Corporation of India)

IFCI is a government-backed financial institution that has been working on cleaning up its balance sheet. Over the past few years, the company has focused on reducing non-performing assets (NPAs) and improving asset quality.

- Financial Snapshot: Gradual improvement in net profit and reduction in bad loans

- Recent Growth: Better recovery from stressed assets and improved capital adequacy

- Competitive Edge: Strong government backing and potential benefit from PSU reforms

- Risk Factor: Still dependent on asset recovery and policy support

Unitech

Unitech is a real estate company that has gone through major financial and legal challenges. However, recent developments have brought it back into investor discussions.

- Financial Snapshot: Weak balance sheet but undergoing restructuring under government supervision

- Recent Growth: Revival efforts through project completion and asset monetization

- Competitive Edge: Large land bank in prime locations

- Risk Factor: Execution delays and past legal issues still impact investor confidence

Both stocks are not typical growth stories but high-risk, high-reward turnaround bets. Investors looking at these should closely track quarterly updates, debt reduction progress, and management actions before making any decision.

Public Opinion: What Real Investors Are Saying

This is where things get interesting. From recent discussions and market chatter:

- Many investors are calling Alok Industries a “sleep-on-it stock”

- Zomato is being seen as a long-term consumption play

- Trident investors are divided due to short-term pressure

- Small-cap manufacturing stocks are being called “hidden gems”

The common mindset is very clear:

People are ready to hold till 2030. But they also know the risks.

How To Identify High Potential Penny Stocks (Real Strategy)

Instead of blindly investing, here’s what actually works:

- Promoter Strength: If strong promoters are involved, chances of survival increase.

- Sector Growth: Always pick sectors that are growing. Not dying ones.

- Debt Situation: Turnaround stories only work if debt reduces over time.

- Business Model: Simple rule. If you don’t understand the business, skip it.

- Volume And Liquidity: Low liquidity can trap your money. Always check this.

Risks You Should Not Ignore

Let’s be real. Penny stocks are not easy money. Here are the main risks:

- High volatility

- Low transparency

- Sudden price manipulation

- Poor financials

- Liquidity issues

Even a small negative news can crash the stock. So never go all-in.

My Final Words On High Growth Penny Stocks

The hype around best penny stocks with high growth potential is definitely real, and it’s easy to get excited when you see stories of people making huge returns. But if I’m being honest with you, the real game here is patience and discipline.

Stocks like Alok Industries, Trident, Zomato, and others might look promising, but they are not guaranteed winners. They are simply part of a bigger picture India’s long-term growth story. And that story will take time to unfold.

If even a few of these companies manage to execute well, the rewards can be truly life-changing. But at the same time, things don’t always go as planned in the market, and losses can happen too.

So my personal advice would be this don’t rush, don’t follow hype blindly, and never invest money you can’t afford to lose. Take your time to understand the business, stay patient, and think long term. That’s how you give yourself the best chance to actually benefit from these opportunities.

Related Posts :

Share This Post