Rajputana Stainless Share Price Target 2030: A Complete Guide for Long-Term Investors

Rajputana Stainless Share Price Target 2030

Rajputana Stainless Share Price Target 2030: Rajputana Stainless is a Gujarat-based stainless steel manufacturer that has been in business for over 30 years. The company produces billets, ingots, round bars, hex bars, square bars, wire rods, and flat bars.

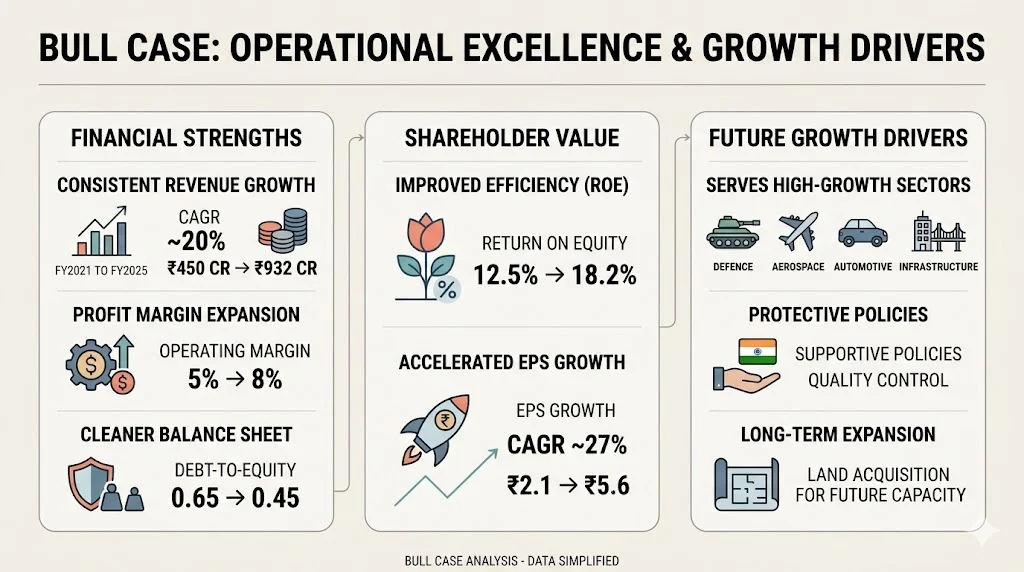

The company recently listed on the stock exchanges in March 2026 after raising ₹254.98 crore through its IPO. Revenue has grown from around ₹450 crore in FY2021 to ₹932 crore in FY2025, which is a CAGR of nearly 20%. Net profit improved from ₹15 crore to ₹39.8 crore in the same period, showing a CAGR of around 27%.

The debt-to-equity ratio has also come down from 0.65 in FY2021 to 0.45 in FY2025. Promoter holding stands at 57% post IPO, which indicates continued confidence from the management team.

In this blog post we are going to see the Share Price Target of Rajputana Stainless from 2026-2030 with the help of numeric and fundamental data and try to guess how much returns can you expect from this share in upcoming years.

Table of Contents

Rajputana Stainless Share Price Target 2026

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 87 | 190 |

| December | 190 | 271 |

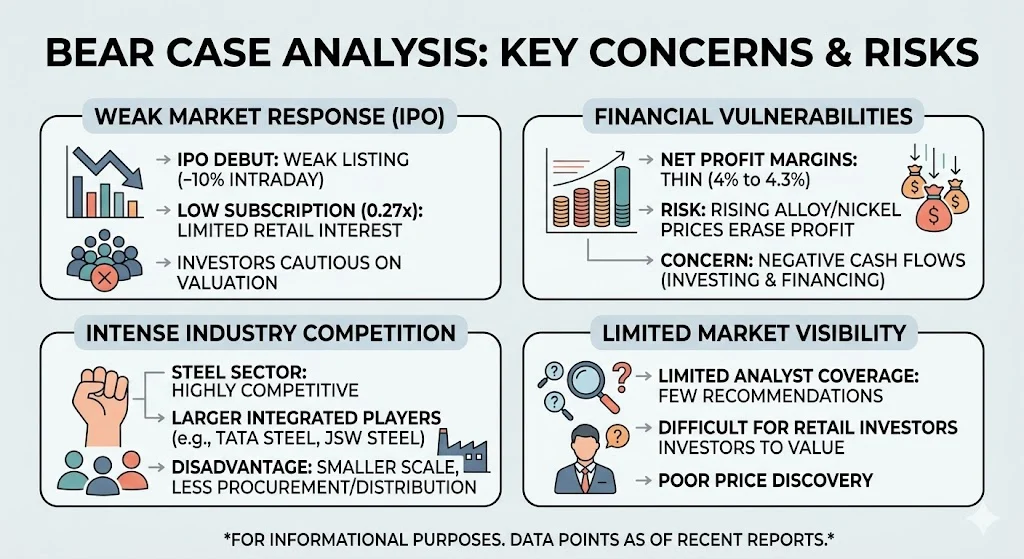

The year 2026 is a foundation year for Rajputana Stainless. The company just completed its IPO in March 2026 at a price band of ₹116 to ₹122 per share. The listing was muted. Shares debuted at around ₹123.95 on BSE and fell nearly 10% intraday shortly after. This kind of weak listing is common for newly listed small-cap companies in cyclical sectors.

The IPO proceeds are being used for two purposes. First, for capacity expansion through a new land acquisition worth ₹18 crore in Gujarat. Second, for partial debt repayment which will reduce interest burden going forward. These are the right moves for a company at this stage of growth.

The government’s push on infrastructure and the Make in India initiative is creating consistent demand for stainless steel products. Rajputana Stainless is well positioned in this space. The company supplies to multiple industries so revenue is not dependent on a single sector.

However, 2026 also carries risks. Post-IPO price correction, limited analyst coverage, and raw material price volatility are key concerns. The Q3 FY26 results, scheduled to be reviewed in the April 9 board meeting, will be an important trigger for the stock. If results show margin improvement, sentiment can turn more positive.

Investors who want to enter this stock in 2026 should wait for the results and monitor how the stock behaves near support levels of ₹110 to ₹115. Rushing into a freshly listed small-cap without watching at least one or two quarters of results can increase risk unnecessarily.

Rajputana Stainless Share Price Target 2027

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 255 | 350 |

| December | 322 | 445 |

By 2027, the company’s expansion plans should start showing early results. The new land acquisition in Gujarat will likely be operational by this time. Increased production capacity means the company can serve more clients and grow its export book.

One key advantage Rajputana Stainless has is its export diversity. It sells to UAE, USA, Turkey, Kuwait, and Poland. This spread reduces dependence on domestic demand cycles. When domestic demand is slow, export orders can fill the gap. This is an important cushion for a small-cap manufacturer.

The operating profit margin reached 8% in FY2025, up from 5% in FY2021. This shows the company is getting better at managing its cost structure over time. If this improvement continues, margins can push past 9% by 2027.

The stainless steel sector in India is also supported by government quality control orders that mandate BIS certification. These orders reduce the threat from low-quality imports. This regulation directly benefits domestic manufacturers like Rajputana Stainless.

The main risks to watch in 2027 are nickel and alloy price movements. Nickel is a key raw material for stainless steel. Any sharp rise in global nickel prices can compress margins quickly. Investors should track global commodity trends alongside company results.

Also Read

Gold Prices Drop Today: 7 Big Reasons Behind The Fall And What Investors Should Watch Next

Rajputana Stainless Share Price Target 2028

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 437 | 550 |

| December | 520 | 644 |

By 2028, Rajputana Stainless should be operating at a higher scale. The factory in Panchmahal currently has a melting capacity of 48,000 tons and a rolling capacity of 36,000 tons per year. New investments from IPO proceeds and internal cash flows can push these numbers higher.

The company’s product range is already wide. It makes round bars, square bars, hex bars, wire rods, and flat bars. These products serve construction, automotive, oil and gas, aviation, and defence sectors. All of these industries are on a growth path in India. Defence indigenization is expanding rapidly. Aviation is growing fast. These are long-term tailwinds.

The Union Budget 2025-26 continued to offer nil basic customs duty on key raw materials like ferro-nickel and ferrous scrap. This helps domestic manufacturers manage input costs better and compete with imported steel products.

Financially, if the company maintains its 20% revenue CAGR, revenue could approach ₹1,600 to ₹1,800 crore by FY2028. Net profit, growing at 27% CAGR, could reach around ₹80 to ₹90 crore by the same period. These numbers would make the valuation more comfortable at that point.

Margins will be the key thing to watch. The company currently earns around 4 to 4.3% net profit margin. For the stock to move strongly toward the upper end of the 2028 target range, margins need to improve toward 5.5% or above.

Rajputana Stainless Share Price Target 2029

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 620 | 750 |

| December | 700 | 870 |

By 2029, Rajputana Stainless is likely to enter a mature growth phase. Expansion projects initiated in 2026 should be fully operational. This means the company can achieve better economies of scale. Larger volumes help spread fixed costs and improve profitability.

The debt-to-equity ratio has been steadily improving. It was 0.65 in FY2021 and reached 0.45 by FY2025. Part of the IPO proceeds are earmarked for further debt reduction. If this trend continues, the D/E ratio could fall below 0.30 by 2029. Lower debt means lower interest costs and better net profit margins.

The stainless steel industry is cyclical. During strong economic periods, demand from construction and industrial sectors rises sharply. If India’s GDP continues growing at 6 to 7% annually, demand for steel products will follow. Rajputana Stainless is positioned to benefit from this macro trend.

The company’s EPS has grown from ₹2.1 in FY2021 to ₹5.6 in FY2025. At a 27% profit CAGR, EPS could cross ₹18 to ₹20 by FY2029. This kind of EPS growth, combined with improving ROE, can attract more institutional interest in the stock over time.

The risk in 2029 remains the cyclical nature of steel. A global slowdown or a sharp correction in commodity prices can affect both revenue and margins. Investors with a long-term view should use any such correction as an opportunity to accumulate.

Rajputana Stainless Share Price Target 2030

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 840 | 1000 |

| December | 1125 | 1280 |

The year 2030 is the most important long-term target for most investors searching this keyword today. Here is what the picture looks like at that point if the company executes well.

By 2030, Rajputana Stainless could become a well-established mid-cap steel manufacturer. Revenue at a 20% CAGR from the 2025 base of ₹932 crore would cross ₹2,300 crore by FY2030. Profit at a 27% CAGR could cross ₹130 crore. This would significantly re-rate the company’s valuation from its current small-cap status.

The company serves defence, aerospace, automotive, and oil and gas sectors. All of these sectors are on a strong long-term growth path in India. The government’s defence self-reliance push means more domestic sourcing of specialty steel components. Rajputana Stainless already has clients in this space and can grow these relationships over the next five years.

The Khavda renewable energy park in Gujarat and similar large infrastructure projects will drive sustained demand for construction grade stainless steel. The company’s geographical proximity to these projects in Gujarat gives it a supply chain advantage.

Export growth is another key driver. The company already sells to five international markets. Stainless steel demand is growing globally, especially in markets like the USA and Middle East. If Rajputana Stainless can grow its export share from 15 to 20% of revenue to 25 to 30% by 2030, it will significantly de-risk the business.

However, to reach the upper end of the 2030 target range, the company needs to improve net profit margins from the current 4.3% to at least 6%. This requires better product mix, higher value-added products, and steady raw material cost management. If margins stay flat, the stock may remain closer to the lower end of the target range.

Overall, 2030 represents a strong potential year for Rajputana Stainless. The foundation is being laid now through the IPO, expansion, and debt reduction. Investors who enter at a reasonable price and hold with patience through the ups and downs of the steel cycle can see meaningful returns.

Rajputana Stainless Share Price Target 2040

By 2040, Rajputana Stainless has the potential to become a major name in the Indian stainless steel space. The share price target for 2040 is expected to be in the range of ₹2,147 to ₹2,541.

India’s industrial and infrastructure growth over the next 15 years will drive massive demand for stainless steel. Sectors like metro rail, water management, food processing, pharmaceuticals, and chemical plants all require high-grade stainless steel. Rajputana Stainless is already present in most of these end markets.

By 2040, the company may also shift toward more value-added products. Higher value products carry better margins. This can lift net profit margins significantly above the current 4 to 4.3% range. A move toward specialty grades and precision steel can open new revenue streams.

Sustainability will also become a major factor. Companies using electric arc furnaces and scrap-based production will have lower carbon footprints. Rajputana Stainless already uses induction furnaces which are more energy efficient. Continuing to invest in cleaner technology can strengthen its position with ESG-conscious institutional investors by 2040.

Rajputana Stainless Share Price Target 2050

The share price target for 2050 is expected to range between ₹4,512 and ₹4,985.

At this point, the company’s trajectory depends entirely on how well it adapts to changing market conditions. The Indian economy is expected to be the world’s third largest by 2050. Demand for all forms of steel will be several times what it is today. A company with a 30-plus year track record and consistent expansion focus is well positioned to capture a share of this growth.

Innovation will be the key differentiator by 2050. Companies that invest in automation, AI-driven quality control, and green manufacturing will lead the sector. Rajputana Stainless will need to evolve its production capabilities to stay competitive at that horizon.

For investors thinking about 2050, the entry point matters much less than the holding conviction. Compounding works powerfully over 25-year periods in fundamentally sound businesses.

Should I Buy Rajputana Stainless Share?

Rajputana Stainless is focused on capacity expansion, debt reduction, and serving high-growth sectors in India. The IPO funds are being deployed wisely. The management has run this business for over 30 years which shows they understand the industry well.

The company is investing in a new manufacturing facility in Gujarat. It is targeting both domestic and export markets. The stainless steel sector has long-term demand visibility thanks to infrastructure spending and industrial growth in India.

That said, the stock is newly listed and has shown weak post-IPO performance. The steel sector is cyclical and margins are thin. Raw material price spikes can hurt profitability in any given year.

Before investing, you should track at least two quarters of post-IPO financial results. Watch how management handles raw material cost pressures. Check whether margins are improving or declining. Understand that this is a long-term story and short-term volatility will be high.

Do your own research before making any investment decision. Every investment carries risk and past growth does not guarantee future returns.

Is Rajputana Stainless Stock Good to Buy? Bull Case and Bear Case

Bull Case

- Revenue has grown at a 20% CAGR from FY2021 to FY2025, going from ₹450 crore to ₹932 crore. This is a strong and consistent track record for a company in a commodity sector. Profit has grown even faster at around 27% CAGR, which shows that operational efficiency is improving along with scale.

- Operating profit margin improved from 5% in FY2021 to 8% in FY2025. This trend shows that the company is getting better at cost management as it grows. The debt-to-equity ratio has declined from 0.65 to 0.45, which means the balance sheet is getting cleaner every year.

- ROE has improved from 12.5% in FY2021 to 18.2% in FY2025. A rising ROE shows that the company is generating better returns on shareholder money each year. EPS has also grown from ₹2.1 to ₹5.6 in the same period.

- The company serves multiple high-growth sectors including defence, aerospace, automotive, and infrastructure. Government policies like Make in India and quality control orders protect domestic manufacturers from cheap imports. The new land acquisition for expansion shows the management is thinking long-term.

Bear Case

- The IPO listing was weak and the stock fell around 10% intraday after debut. This shows that investors are cautious about the valuation at current levels. The overall IPO subscription was only 0.27 times, which is very low. This reflects limited retail interest in the stock.

- Net profit margins are thin at around 4 to 4.3%. Any rise in nickel or alloy prices can quickly erase profitability. The company has negative cash flows from investing and financing activities in recent periods which is a concern for a growing business that needs capital.

- The steel sector is highly competitive. Large integrated players like Tata Steel and JSW Steel have far greater scale, better procurement power, and larger distribution networks. Competing with them for institutional clients will not be easy.

- Limited analyst coverage means there are very few formal buy or sell recommendations available. This makes price discovery harder for retail investors.

Promoter Holding Of Rajputana Stainless

| Period | Promoter Holding % |

|---|---|

| Pre-IPO (FY2025) | 72.5% |

| Post-IPO (March 2026) | 57.0% |

| Current (April 2026) | 57.0% |

Promoter holding reduced from 72.5% to 57% as part of the IPO process. The OFS component of the IPO was ₹76.25 crore, through which promoters sold a portion of their stake.

A 57% promoter holding post-IPO is still a strong number. It shows that promoters continue to hold the majority stake even after going public. High promoter holding generally means the owners have skin in the game. They are not fully exiting. They still believe in the long-term potential of the business.

However, investors should watch whether promoter holding declines further in coming quarters. Any significant promoter selling after the lock-in period expires can put pressure on the stock price. As long as holding stays above 50%, the management signal remains positive.

For a company that has been privately run for over 30 years, maintaining 57% ownership after an IPO is a reasonable and healthy sign.

Revenue Growth of Rajputana Stainless

| Financial Year | Revenue (₹ Crore) | YoY Growth % |

|---|---|---|

| FY2021 | 450 | — |

| FY2022 | 520 | 15.6% |

| FY2023 | 650 | 25.0% |

| FY2024 | 780 | 20.0% |

| FY2025 | 932 | 19.5% |

Revenue has grown consistently from ₹450 crore in FY2021 to ₹932 crore in FY2025. The 5-year CAGR is approximately 20%. This is a strong revenue growth rate for a stainless steel manufacturer in a competitive market.

The growth was particularly strong in FY2023, when revenue jumped 25%. This coincided with the post-pandemic industrial recovery and a surge in infrastructure activity in India. Growth moderated slightly in FY2024 and FY2025 as the base got larger and competition increased.

For a company generating nearly ₹1,000 crore in revenue, the next milestone will be reaching ₹1,500 crore. Achieving this will depend on successful execution of the capacity expansion and continued export growth. The domestic market remains the primary driver but export diversification can add meaningful revenue going forward.

Compared to the broader steel sector average revenue CAGR of around 12 to 15%, Rajputana Stainless has outperformed. This suggests the company has been gaining market share steadily.

Profit Growth of Rajputana Stainless

| Financial Year | Net Profit (₹ Crore) | YoY Growth % |

|---|---|---|

| FY2021 | 15 | — |

| FY2022 | 20 | 33.3% |

| FY2023 | 28 | 40.0% |

| FY2024 | 35 | 25.0% |

| FY2025 | 39.8 | 13.7% |

Profit has grown at a 5-year CAGR of around 27%. This is faster than revenue growth of 20%, which means the company is becoming more efficient over time. When profit grows faster than revenue, it is a sign that operating leverage is working.

The highest profit growth was in FY2023 when profit jumped 40%. This was driven by improved operating margins and better product mix. However, growth moderated in FY2025 to around 13.7%. This moderation is worth watching.

Compared to revenue, profit growth has started to slow. If raw material costs rise or competition increases pricing pressure, profit growth could slow further. Management focus on moving toward higher value-added products will be key to sustaining above-average profit growth rates.

EPS and ROE Trends of Rajputana Stainless

| Financial Year | EPS (₹) | ROE % |

|---|---|---|

| FY2021 | 2.1 | 12.5 |

| FY2022 | 2.8 | 14.2 |

| FY2023 | 3.9 | 16.8 |

| FY2024 | 4.9 | 17.5 |

| FY2025 | 5.6 | 18.2 |

EPS has grown from ₹2.1 in FY2021 to ₹5.6 in FY2025. This is a strong and steady rise. It tells you that the company is generating more profit per share each year.

ROE has moved from 12.5% to 18.2% in the same period. A rising ROE is one of the best indicators of a healthy business. It means the company is getting better at using shareholder money to generate profits. An ROE above 15% is generally considered good for a manufacturing company. Rajputana Stainless has crossed this benchmark and is moving higher.

For long-term investors, the combination of rising EPS and rising ROE is a positive signal. It suggests that growth is not just coming from debt-funded expansion but from genuine improvement in business efficiency.

If the company can push ROE toward 20% or above by FY2027 or FY2028, it will attract more institutional investor interest which can support the stock price.

Debt-to-Equity Ratio of Rajputana Stainless

| Financial Year | Debt-to-Equity Ratio |

|---|---|

| FY2021 | 0.65 |

| FY2022 | 0.58 |

| FY2023 | 0.52 |

| FY2024 | 0.48 |

| FY2025 | 0.45 |

The debt-to-equity ratio has declined every single year from 0.65 in FY2021 to 0.45 in FY2025. This is a very encouraging trend. It tells you that the company is reducing its dependence on borrowed money even while it continues to grow.

For a steel manufacturer, a D/E ratio below 0.5 is considered comfortable. The company has crossed this threshold and is continuing to improve. Part of the IPO proceeds are also being used for debt repayment, which will bring this ratio down further in FY2026.

Lower debt means lower interest payments each year. This directly improves net profit. It also makes the company more resilient during economic downturns when revenues may fall but fixed obligations remain.

If the D/E ratio falls below 0.30 by FY2028 or FY2029, the company will have a very clean balance sheet. This kind of financial discipline is rare in the commodity manufacturing sector and deserves credit.

Net Profit Margin of Rajputana Stainless

| Financial Year | Net Profit Margin % |

|---|---|

| FY2021 | 3.3 |

| FY2022 | 3.8 |

| FY2023 | 4.3 |

| FY2024 | 4.5 |

| FY2025 | 4.3 |

Net profit margins have improved from 3.3% in FY2021 to around 4.3% to 4.5% in recent years. The improvement is real but the absolute level is still thin. For a stainless steel manufacturer, margins in the 4 to 5% range are fairly standard given the commodity nature of the business.

The margin plateaued between FY2024 and FY2025. This signals that there is a ceiling to how much cost efficiency can do on its own. To push margins meaningfully higher, the company needs to either increase the share of higher-value products or grow the export mix toward premium markets.

The operating profit margin tells a more positive story. It improved from 5% in FY2021 to 8% in FY2025. The gap between operating margin and net margin is being compressed by interest costs and tax. As debt reduces and interest costs fall, more of the operating profit will flow down to the net profit line.

Investors should track this ratio closely every quarter. Any sustained improvement above 5% net margin would be a meaningful positive for the stock.

Market Capitalization of Rajputana Stainless

| Period | Market Capitalization |

|---|---|

| IPO Price (March 2026) | ~₹700 Crore |

| Current (April 2026) | ~₹990 Crore |

Rajputana Stainless is currently a small-cap company with a market cap of around ₹990 crore. At this size, the stock has the potential for significant re-rating if the company continues to grow at its current pace.

Small-cap stocks in India can deliver exceptional returns when they transition from small-cap to mid-cap. The threshold for mid-cap classification in India is roughly ₹5,000 crore in market cap. For Rajputana Stainless to reach this level, it would need its stock to grow roughly 5 times from current levels.

This kind of move is possible over a 5 to 7 year period if revenue grows at 20% CAGR and margins improve. However, the path will not be linear. Small-cap stocks face higher volatility, lower liquidity, and are more sensitive to market sentiment.

The current market cap also reflects cautious investor sentiment post-IPO. As the company starts delivering quarterly results and demonstrating post-IPO growth, the market cap can start to reflect fundamental value more accurately.

Dividend Yield of Rajputana Stainless

| Year | Dividend Yield |

|---|---|

| FY2021 to FY2025 | 0% |

| Current (2026) | 0% |

Rajputana Stainless has not paid any dividend since inception. The company reinvests all its profits back into the business for expansion and debt reduction. This is a common strategy for growth-stage companies.

For income-seeking investors, this stock is not the right choice. There is no dividend yield to compensate for the risk.

For growth investors, the zero dividend policy is acceptable as long as the retained profits are being deployed effectively. The company’s consistent revenue and profit growth suggests that retained earnings are being put to productive use.

If the company reaches a stable growth phase by FY2030, it may consider introducing a dividend. But for now, investors should not expect any dividend income from this stock. The investment case here is entirely based on capital appreciation.

Conclusion On Rajputana Stainless

Rajputana Stainless is a well-run stainless steel manufacturer with a 30-year track record and improving financial metrics. Revenue CAGR of 20%, profit CAGR of 27%, rising ROE, and declining debt all point toward a business that is executing well.

The recent IPO in March 2026 gave the company access to growth capital. The funds are being deployed for capacity expansion in Gujarat and debt reduction. These are the right priorities for a company at this stage.

The share price target for 2030 of ₹840 to ₹1,280 is achievable if the company maintains its growth trajectory and improves its net profit margins toward 5.5% or above. Sectors like defence, aerospace, automotive, and infrastructure will continue to create demand for stainless steel products in India over the next five years.

Always do your own research before investing. Understand your risk appetite and never invest money you cannot afford to stay invested in for the long term.

Related Posts :

Share This Post