Alok Industries Share Price Target 2026, 2027, 2028, 2029, 2030, 2040, 2050

Alok Industries Share Price Target

Alok Industries is one of India’s leading textile manufacturing companies with presence across the entire value chain such as polyester yarn, cotton yarn, apparel fabrics, home textiles, and garments. The company exports a significant portion of its products and also serves domestic markets. It is backed by Reliance Industries, which holds a strong stake and provides financial support.

Over the last five years, the company has shown volatile performance. Revenue increased sharply to ₹7373 Cr in FY22 but declined continuously to ₹3709 Cr in FY25. The company is still making losses, although losses have reduced compared to earlier years. The stock is currently trading near ₹12–13 and is close to its 52-week low, reflecting weak investor confidence.

In this blog post we are going to see the share price target of the alok industries share by seeing the fundamentals & numeric data. And try to estimate how much returns can you expect from this share in upcoming years. So Keep reading..

Table of Contents

Alok Industries share price target 2026

| Month | Share Price Target |

|---|---|

| January 2026 | ₹12 – ₹15 |

| December 2026 | ₹14 – ₹20 |

In 2026, the company’s performance will depend on recovery in textile demand and improvement in margins. Recent quarterly results show that losses are reducing, which is a positive sign. However, the company is still not profitable. Textile sector demand is slowly improving and government schemes like PLI can support growth. Still, weak fundamentals may limit sharp upside.

Alok Industries share price target 2027

| Month | Share Price Target |

|---|---|

| January 2027 | ₹15 – ₹20 |

| December 2027 | ₹20 – ₹28 |

By 2027, the company may benefit from export demand and improvement in global textile markets. Around 24% of revenue comes from exports, especially from the US. If demand improves and cost control is better, losses may reduce further. Reliance backing also provides stability, which can support long-term recovery.

Alok Industries share price target 2028

| Month | Share Price Target |

|---|---|

| January 2028 | ₹18 – ₹25 |

| December 2028 | ₹28 – ₹38 |

In 2028, growth may improve if the company achieves breakeven or small profit. Vertical integration in textile operations can help reduce costs and improve margins. Government support for textile manufacturing and exports can also act as a positive factor. However, competition in textile sector remains high.

Alok Industries share price target 2029

| Month | Share Price Target |

|---|---|

| January 2029 | ₹25 |

| December 2029 | ₹40 |

By 2029, the company may show stable growth if profitability improves. Textile demand in India and global markets can support revenue growth. But the company needs to manage costs and improve efficiency to sustain growth.

Alok Industries share price target 2030

| Month | Share Price Target |

|---|---|

| January 2030 | ₹35 |

| December 2030 | ₹55 |

In 2030, long term growth depends on consistent profitability and strong demand. If the company successfully improves margins and reduces losses, it can see better valuation. Reliance backing remains a key support factor.

Alok Industries share price target 2040

| Month | Share Price Target |

|---|---|

| January 2040 | ₹90 |

| December 2040 | ₹150 |

By 2040, the company’s success will depend on its ability to compete globally and adapt to sustainable textile trends. Export growth and innovation will be key drivers.

Alok Industries share price target 2050

| Month | Share Price Target |

|---|---|

| January 2050 | ₹220 |

| December 2050 | ₹350 |

In 2050, long term growth depends on strong execution and financial discipline. Textile industry will continue to grow, but only efficient companies will benefit.

Should I buy Alok Industries share?

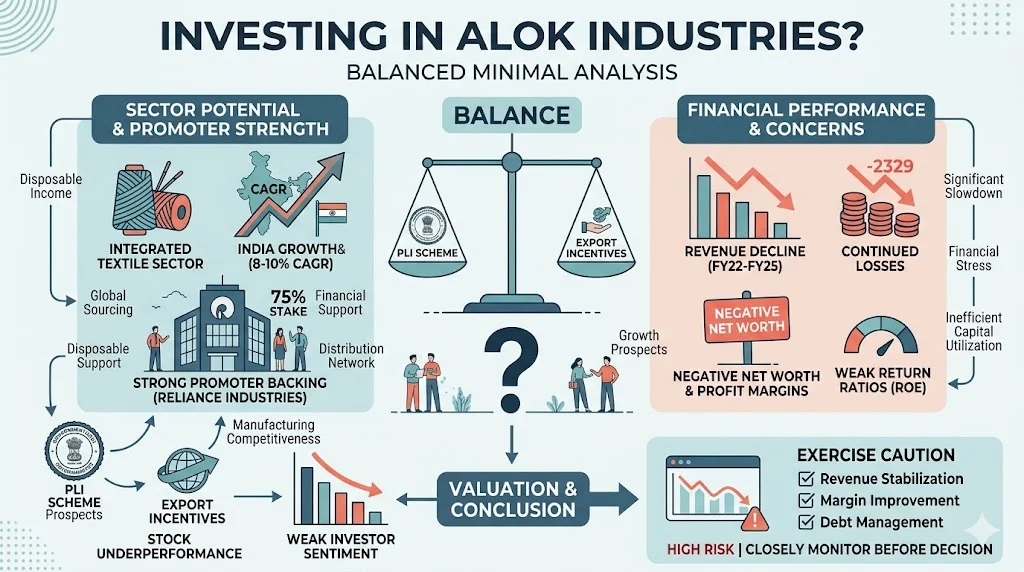

Alok Industries Limited operates in the integrated textile sector, covering polyester yarn, cotton yarn, apparel fabrics, and home textiles, which positions it to benefit from India’s growing domestic consumption and export demand. The Indian textile industry is expected to grow at a CAGR of 8–10% over the next decade, supported by rising disposable income, urbanization, and global sourcing shifts.

The company also benefits from strong promoter backing, with Reliance Industries holding a 75% stake, providing financial support, operational stability, and access to a wider distribution network. Additionally, government initiatives such as the Production Linked Incentive (PLI) scheme and export incentives are expected to boost manufacturing competitiveness and improve long-term growth prospects.

However, the company’s financial performance remains a key concern. Revenue has declined from ₹7,373 Cr in FY22 to ₹3,709 Cr in FY25, indicating a significant slowdown in business activity. The company continues to report losses, with net loss of ₹816 Cr in FY25, and maintains a negative net worth, which reflects financial stress. Profit margins remain negative, and return ratios such as ROE are weak, indicating inefficient capital utilization. Despite promoter support, the company has not yet demonstrated a clear turnaround in profitability.

The stock has also underperformed, trading near its lower range, reflecting weak investor sentiment and limited confidence in near-term recovery. While the long-term industry outlook remains positive, the company’s current fundamentals suggest high risk. Investors should closely monitor revenue stabilization, margin improvement, and debt management before considering any investment decision.

Also Read: Best Penny Stocks With High Growth Potential: 10 Hidden Multibaggers For 2030 You Should Watch

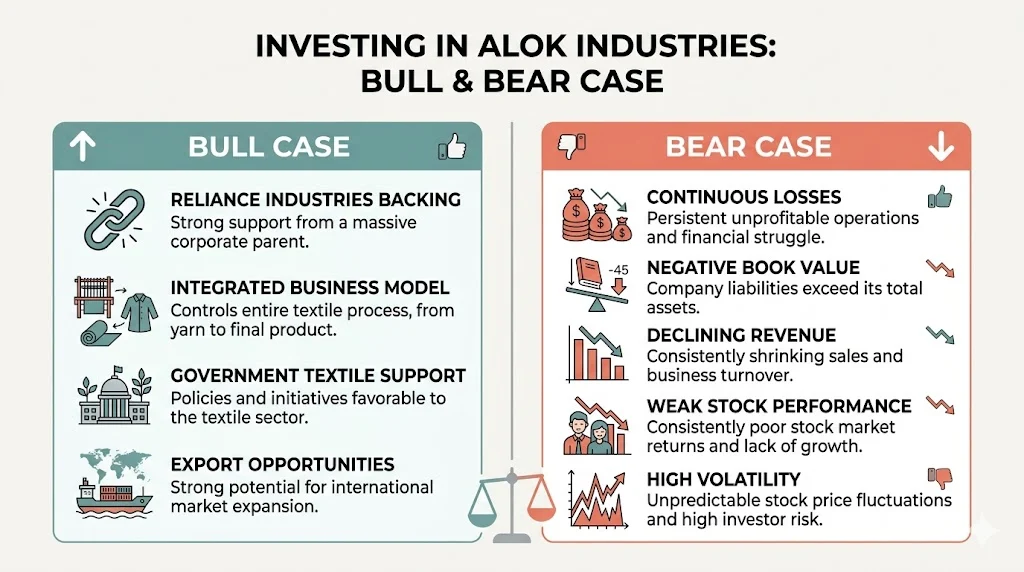

Is Alok Industries stock good to buy (Bull case & Bear case):

Bull case:

- Strong backing from Reliance Industries

- Integrated textile business model

- Government support for textile sector

- Export opportunities

Bear case:

- Continuous losses

- Negative book value

- Declining revenue

- Weak stock performance

- High volatility

Promoters Holding Of Alok Industries

| Period | Holding |

|---|---|

| Mar 2021 | 75% |

| Mar 2022 | 75% |

| Mar 2023 | 75% |

| Mar 2024 | 75% |

| Mar 2025 | 75% |

Promoter holding is stable at 75%, which is a positive sign. It shows strong control and confidence of promoters in the company. Since Reliance Industries is a major promoter, it adds stability and trust. Stable promoter holding over many years indicates long-term commitment towards the business. However, investors should also focus on financial performance because high promoter holding alone cannot guarantee returns.

Revenue growth Of Alok Industries

| Year | Revenue (₹ Cr) |

|---|---|

| 2021 | 3885 |

| 2022 | 7373 |

| 2023 | 6989 |

| 2024 | 5510 |

| 2025 | 3709 |

Revenue shows a declining trend after FY22. The company saw strong growth in FY22 when revenue reached ₹7373 Cr, but after that it started falling continuously to ₹3709 Cr in FY25. This decline indicates weak demand or operational challenges. It also shows that the company is not able to maintain its growth momentum.

Profit growth (CAGR%) of Alok Industries

| Year | Net Profit (₹ Cr) |

|---|---|

| 2021 | -5673 |

| 2022 | -209 |

| 2023 | -880 |

| 2024 | -847 |

| 2025 | -816 |

The company is still making losses. Although losses reduced significantly from FY21 to FY22, they increased again in later years. Continuous losses are a major concern. It shows that the company is not able to generate profit despite large revenue.

EPS or ROE trends of Alok Industries

| Year | EPS | ROE |

|---|---|---|

| 2021 | -11.43 | 32.13% |

| 2022 | -0.42 | 1.16% |

| 2023 | -1.77 | 4.66% |

| 2024 | -1.71 | 4.28% |

| 2025 | -1.64 | 3.96% |

EPS is negative in all years, which clearly reflects that the company has been continuously making losses and is not able to generate earnings for shareholders.

Although the losses reduced significantly from FY21 to FY22, EPS again deteriorated in the following years, showing that the recovery is not stable. ROE also shows a declining and inconsistent trend, falling from 32.13% in FY21 to around 3.96% in FY25.

This sharp drop indicates that the company is not efficiently using shareholders’ capital to generate returns. Overall, the combination of negative EPS and weak ROE highlights poor financial performance, lack of profitability, and limited value creation for investors.

Use Tools: HDFC SIP Calculator – Easily Plan Your Monthly Investments

Debt-to-equity ratio of Alok Industries

| Year | D/E |

|---|---|

| 2021 | -1.37 |

| 2022 | -1.36 |

| 2023 | -1.28 |

| 2024 | -1.32 |

| 2025 | -1.26 |

Debt-to-equity ratio is negative due to negative net worth, which means the company’s liabilities are higher than its total equity. This situation usually arises when a company has accumulated losses over time, eroding its shareholder equity. In the case of Alok Industries, continuous losses in recent years have led to this negative net worth position.

A negative D/E ratio is a strong indicator of financial stress, as it reflects weak balance sheet strength and higher dependence on external funding. It also increases the risk for investors because the company may face challenges in raising fresh capital or servicing its obligations. Although the backing of Reliance Industries provides some level of financial support and stability, the company still needs to improve profitability and rebuild its net worth to reduce this risk in the long term.

Net profit margins of Alok Industries

| Year | Margin |

|---|---|

| 2021 | -147.1% |

| 2022 | -2.8% |

| 2023 | -12.6% |

| 2024 | -15.4% |

| 2025 | -22.0% |

Margins are negative in all years, which clearly indicates that the company has not been able to generate profits from its operations. In FY21, the margin was extremely low at -147.1%, showing heavy losses, although it improved significantly to -2.8% in FY22 due to better cost control and higher revenue.

However, after that, margins again deteriorated to -12.6% in FY23, -15.4% in FY24, and further to -22.0% in FY25. This declining trend suggests that the company is struggling with rising costs, weak pricing power, or inefficient operations. Continuous negative margins also indicate that even if revenue is generated, the company is unable to convert it into profit, which is a major concern for long-term investors.

Market capitalization of Alok Industries

| Metric | Value |

|---|---|

| Market Cap | ~₹6,375 Cr |

The company is a mid-cap stock with moderate to high risk.

Dividend yield of Alok Industries

| Year | Dividend | Yield |

|---|---|---|

| 2021 | 0 | 0% |

| 2022 | 0 | 0% |

| 2023 | 0 | 0% |

| 2024 | 0 | 0% |

| 2025 | 0 | 0% |

The company does not pay dividends, so it is not suitable for income investors.

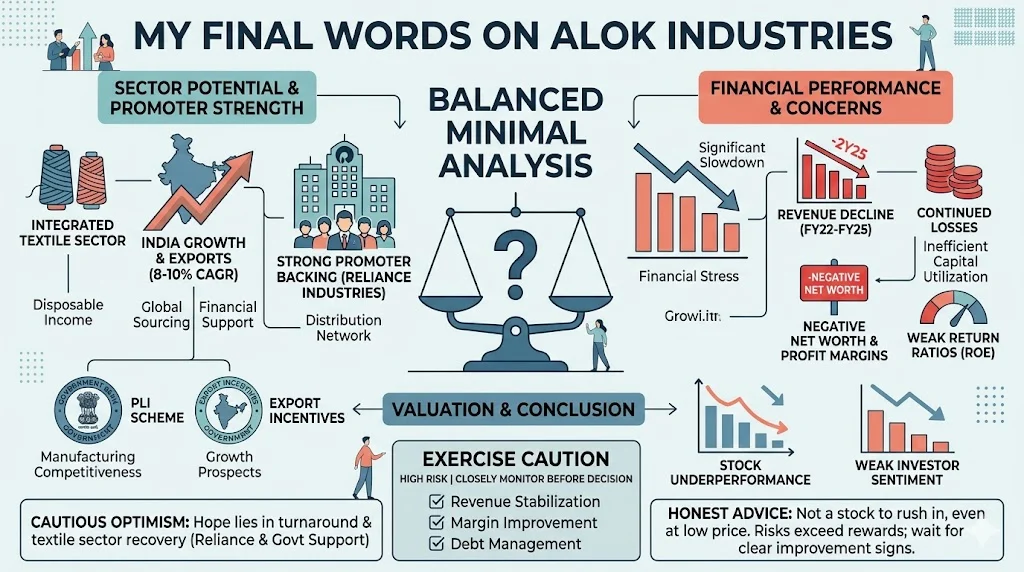

My Final Words On Alok Industries

Alok Industries is a company with strong backing and integrated textile operations, but its financial performance is weak. Declining revenue from ₹7373 Cr in FY22 to ₹3709 Cr in FY25 clearly shows that the company is struggling to maintain demand and scale. Continuous losses, with net loss of around ₹816 Cr in FY25, and consistently negative profit margins highlight serious operational challenges.

The company also has negative net worth, which is reflected in its negative debt-to-equity ratio, indicating financial stress. EPS has remained negative across all years, and ROE is low and inconsistent, showing poor returns for shareholders. However, the company still has some hope if it can improve profitability, control costs, and benefit from a recovery in the textile sector, especially with the support of Reliance Industries and government initiatives.

If I speak honestly, this is not a stock where you should rush in just because the price looks low. Yes, sometimes such stocks can give sharp returns if a turnaround happens, but right now the risks are clearly higher than the rewards. If you are someone who prefers safety and stable growth, it’s better to stay cautious and wait for clear signs of improvement in results.

On the other hand, if you are a high-risk investor and understand the volatility, you can keep this stock on your watchlist and track quarterly performance closely. Look for signs like reducing losses, improving margins, and stable revenue before taking any decision. In simple words, don’t invest based on hope invest based on clear improvement.

Related Posts :

Share This Post