Mishtann Foods Share Price Target 2026, 2027, 2028, 2029, 2030, 2040, 2050

Mishtann Foods Share Price Target 2026, 2027, 2028, 2029, 2030, 2040, 2050

Mishtann Foods is an Indian FMCG company that operates in the food processing sector. The company mainly produces and sells basmati rice, wheat, pulses, and different types of salt such as crystal salt and rock salt.

It was earlier known as HICS Cements Limited and later shifted to the food business to focus on essential consumer products. Over the last five years, the company has shown strong growth in revenue from ₹351.07 Cr in FY21 to ₹348.42 Cr in FY25 with a peak in FY23.

Profit also increased sharply till FY23 but has declined in recent years, which raises concerns. The company is currently facing regulatory issues and weak financial performance, which has impacted investor confidence and stock price significantly.

In this blog post we are going to see the share price target of mistan foods for upcoming year (2026-2050) by seeign the fundamentals, numeric data, etc & try to see how much you can expect from this share if you invested for long term.

Mishtann Foods share price target 2026

| Month | Target Price (₹) |

|---|---|

| January 2026 | 6 – 8 |

| December 2026 | 8 – 12 |

In 2026, the company’s performance will largely depend on how it handles regulatory challenges and improves financial transparency. The recent decline in profit, where Q3 FY26 profit dropped by around 53% YoY, is a negative signal. There are no major new business expansions or product launches announced recently. The company had earlier planned to enter the ethanol business, which could be a growth driver if executed properly. However, current sentiment remains weak due to SEBI restrictions and governance concerns.

Also Read

Gold Prices Drop Today: 7 Big Reasons Behind The Fall And What Investors Should Watch Next

Mishtann Foods share price target 2027

| Month | Target Price (₹) |

|---|---|

| January 2027 | 8 – 12 |

| December 2027 | 10 – 16 |

By 2027, recovery is possible only if the company resolves its regulatory issues and rebuilds investor trust. The company has a strong base in food products like rice and wheat, which are always in demand. Its distribution network across India can support growth. But financial instability and past governance issues will remain a key risk. Investors should closely watch improvements in cash flow and receivables.

Mishtann Foods share price target 2028

| Month | Target Price |

|---|---|

| January 2028 | ₹8 – ₹12 |

| December 2028 | ₹10 – ₹16 |

In 2028, the company may see growth if it successfully expands its product range and improves its supply chain. Demand for branded food products is increasing in India, which can support the company. However, competition from large FMCG companies is very high. Mishtann must focus on cost control and operational efficiency to improve margins.

Mishtann Foods share price target 2029

| Month | Target Price (₹) |

|---|---|

| January 2029 | 12 – 16 |

| December 2029 | 18 – 24 |

By 2029, long term growth will depend on financial discipline and execution. If the company strengthens its balance sheet and reduces risks, it can benefit from rising demand for food products. Expansion into new markets and better branding can also support growth. But the company needs to rebuild credibility in the market.

Mishtann Foods share price target 2030

| Month | Target Price |

|---|---|

| January 2030 | ₹8 – ₹12 |

| December 2030 | ₹15 – ₹22 |

In 2030, the company’s growth potential depends on its ability to stabilize operations and maintain consistent profitability. The food sector has strong demand due to India’s population growth. If Mishtann improves its supply chain and reduces costs, it can achieve better margins. But without strong governance, long term growth may remain uncertain.

Mishtann Foods share price target 2040

| Month | Target Price |

|---|---|

| January | ₹25 |

| December | ₹40 |

By 2040, the company can benefit from global demand for basmati rice and Indian food products. If it builds a strong brand and expands exports, it can grow significantly. But long term success will depend on strong management and financial transparency.

Mishtann Foods share price target 2050

| Month | Target Price (₹) |

|---|---|

| January 2050 | 120 |

| December 2050 | 180 |

In 2050, the company’s future depends on how well it rebuilds trust and scales its operations. The food industry will continue to grow, but only companies with strong governance and efficient operations will succeed. Mishtann must focus on long term stability.

Also Read: High Growth FMCG Stocks In India 2030: 10 Hidden Gems Investors Are Tracking Right Now

Should I buy Mishtann Foods share?

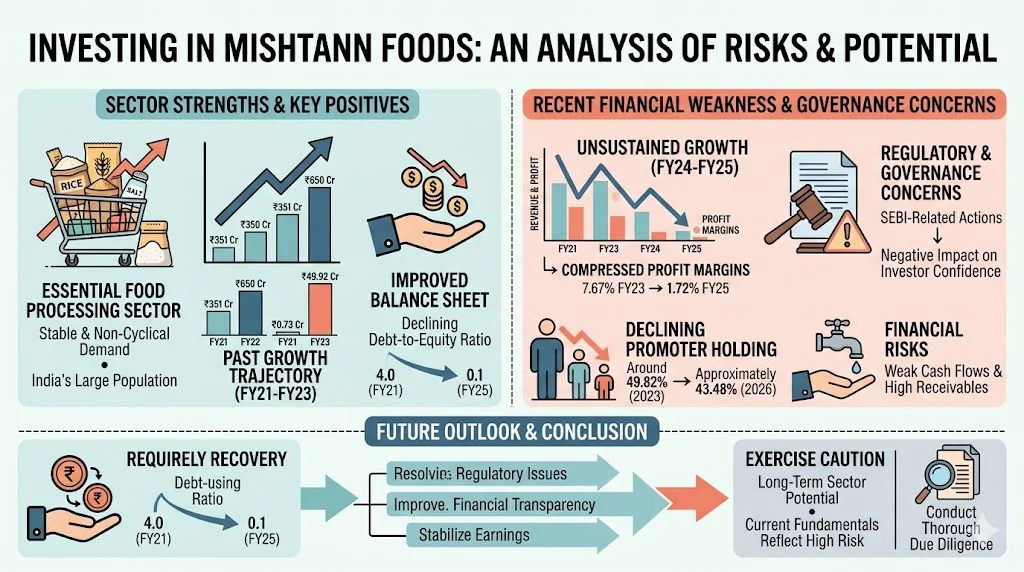

Mishtann Foods operates in the essential food processing sector, which benefits from relatively stable and non-cyclical demand driven by India’s large population and rising consumption of packaged staples such as basmati rice, wheat, and salt.

The company demonstrated strong growth in the past, with revenue increasing from ₹351.07 Cr in FY21 to a peak of ₹650.39 Cr in FY23, and net profit rising sharply from ₹0.73 Cr to ₹49.92 Cr during the same period.

However, this growth has not been sustained, as revenue declined to ₹322.42 Cr in FY24 and marginally recovered to ₹348.42 Cr in FY25, while net profit dropped significantly to ₹5.99 Cr. Profit margins have also compressed from 7.67% in FY23 to 1.72% in FY25, indicating operational inefficiencies and cost pressures.

Additionally, the company is currently facing serious regulatory and governance concerns, including SEBI-related actions, which have negatively impacted investor confidence and stock performance. Promoter holding has declined from around 49.82% in 2023 to approximately 43.48% in 2026, which may raise concerns about long-term commitment.

Although the company has improved its balance sheet by reducing its debt-to-equity ratio from around 4.0 in FY21 to nearly 0.1 in FY25, weak cash flows and high receivables remain key risks.

Going forward, the company’s ability to restore growth will depend on resolving regulatory issues, improving financial transparency, and stabilizing earnings. While the underlying sector offers long-term potential, the current fundamentals reflect high risk. Investors should exercise caution, closely monitor financial performance, and conduct thorough due diligence before considering any investment.

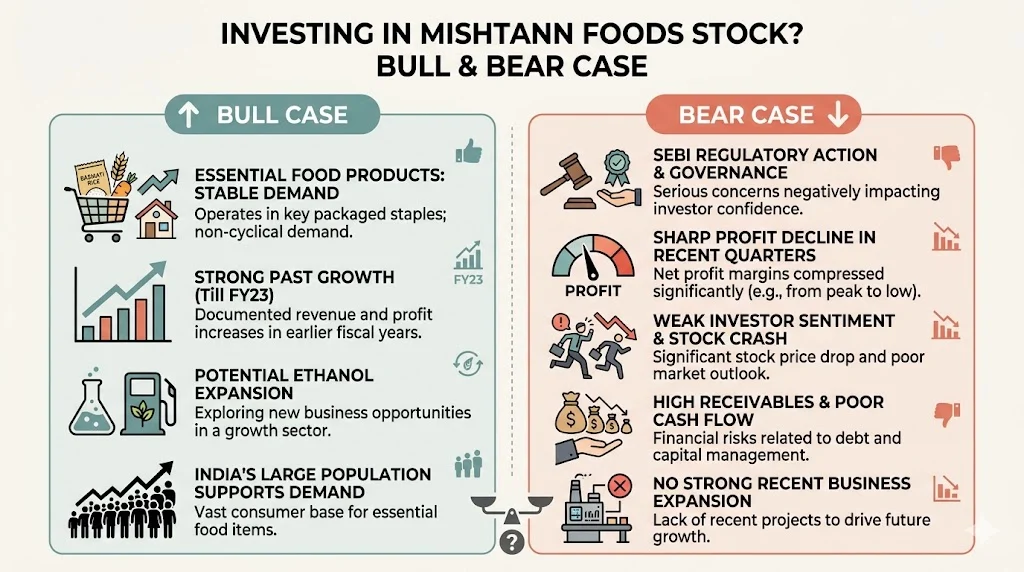

Is Mishtann Foods Stock Good To Buy (Bull case & Bear case)

Bull case:

- Operates in essential food products with stable demand

- Strong past revenue and profit growth till FY23

- Potential expansion into ethanol business

- Large population supports food demand

Bear case:

- SEBI regulatory action and governance issues

- Sharp decline in profit in recent quarters

- Weak investor sentiment and stock crash

- High receivables and poor cash flow

- No strong recent business expansion

Promoters Holding Of Mishtann Foods

| Period | Holding |

|---|---|

| Sep 2023 | 49.82% |

| Mar 2024 | 46.87% |

| Sep 2024 | 43.48% |

| Mar 2025 | 43.48% |

| Mar 2026 | 43.48% |

Promoter holding has declined over the years, which is a negative sign. As seen in the table, the stake has reduced from 49.82% in September 2023 to 46.87% in March 2024 and further down to 43.48% by September 2024, where it has remained stable till March 2026.

This consistent reduction indicates that promoters have been gradually offloading their shares. Such a trend can raise concerns among investors, as it may signal a lack of confidence from the promoters themselves. Lower promoter holding can also increase volatility in the stock and reduce long-term stability, which can negatively impact overall investor sentiment.

Revenue growth Of Mishtann Foods

| Year | Revenue (₹ Cr) |

|---|---|

| 2021 | 351.07 |

| 2022 | 498.58 |

| 2023 | 650.39 |

| 2024 | 322.42 |

| 2025 | 348.42 |

Revenue grew strongly from ₹351.07 Cr in FY21 to ₹650.39 Cr in FY23, showing a clear upward trend during this period. However, in FY24, revenue dropped sharply to ₹322.42 Cr, which indicates a major decline in business performance.

In FY25, there is a slight recovery to ₹348.42 Cr, but it is still far below the peak levels seen in FY23. This fluctuation in revenue over the years clearly shows that the company is facing instability in its growth and is unable to maintain consistent performance.

Profit growth (CAGR%) of Mishtann Foods

| Year | Net Profit (₹ Cr) |

|---|---|

| 2021 | 0.73 |

| 2022 | 31.41 |

| 2023 | 49.92 |

| 2024 | 14.17 |

| 2025 | 5.99 |

Profit increased rapidly till FY23, rising from ₹0.73 Cr in FY21 to ₹49.92 Cr in FY23, which shows strong growth during that period. However, after FY23, profit declined sharply to ₹14.17 Cr in FY24 and further to ₹5.99 Cr in FY25.

This significant drop indicates that the company is facing challenges in maintaining its profitability, highlighting inconsistency in earnings and raising concerns about the sustainability of its growth.

EPS or ROE trends of Mishtann Foods

| Year | EPS | ROE |

|---|---|---|

| 2021 | 0.01 | ~5-12% |

| 2022 | 0.63 | ~23% |

| 2023 | 0.50 | 52.92% |

| 2024 | 0.14 | 100.88% |

| 2025 | 0.06 | 44.1% |

ROE was very high in FY24 at around 100.88%, which indicates that the company generated strong returns on shareholder equity during that year. However, this sharp rise was not sustained, as ROE dropped significantly to around 44.1% in FY25.

Earlier years also show inconsistency, with ROE moving from moderate levels to very high and then declining again. This kind of fluctuation suggests that the company’s profitability is not stable and may be influenced by one-time factors rather than consistent operational performance.

Debt-to-equity ratio of Mishtann Foods

| Year | D/E |

|---|---|

| 2021 | ~4.0 |

| 2022 | ~1.0 |

| 2023 | 0.40 |

| 2024 | 0.09 |

| 2025 | ~0.1 |

Debt has reduced significantly over the years, as seen in the table where the debt-to-equity ratio has come down from around 4.0 in 2021 to nearly 0.1 in 2025.

This sharp decline indicates that the company has actively reduced its reliance on borrowed funds and improved its financial structure. Lower debt reduces interest burden and financial risk, which is a positive sign for the company’s long-term stability.

Net profit margins of Mishtann Foods

| Year | Margin |

|---|---|

| 2021 | 0.21% |

| 2022 | 6.30% |

| 2023 | 7.67% |

| 2024 | 4.40% |

| 2025 | 1.72% |

Margins improved significantly from 0.21% in FY21 to 7.67% in FY23, showing strong operational efficiency and better cost management during that period. However, after FY23, margins declined to 4.40% in FY24 and further dropped to 1.72% in FY25. This sharp fall indicates rising costs, lower pricing power, or inefficiencies in operations, which is putting pressure on the company’s overall profitability.

Market capitalization of Mishtann Foods

| Metric | Value |

|---|---|

| Market Cap | ~₹424 Cr |

The company is a small-cap stock with high risk.

Dividend yield of Mishtann Foods

| Year | Dividend | Yield |

|---|---|---|

| 2021 | 0.00 | 0% |

| 2022 | 0.20 | ~1% |

| 2023 | 0.15 | 0% |

| 2024 | 0.10 | 0% |

| 2025 | 0.00 | 0% |

Dividend is very low and inconsistent as seen in the table above. The company paid ₹0.20 in 2022, which was the highest in recent years, but it dropped to ₹0.15 in 2023 and further to ₹0.10 in 2024. In 2021 and 2025, the company did not pay any dividend at all.

The dividend yield has also remained close to 0% in most years, which shows that shareholders are not getting regular income from the stock. This irregular and minimal dividend history makes it unsuitable for income-focused investors who prefer stable and consistent returns.

Conclusion

Mishtann Foods is one of those stocks that can look attractive at first because of its growth potential, but when you go deeper, you will notice that there are some serious concerns that you simply can’t ignore. Yes, the company operates in a sector that will always have demand, but right now its financial performance and regulatory issues make things quite uncertain. The ups and downs in revenue and profit clearly show that the business is not stable yet, and that’s something every investor should think about carefully.

If the company manages to fix its governance issues and bring consistency in its financials, it can definitely make a comeback in the future. But as of now, this is not a stock you should jump into without thinking.

Personally I want to say that this is only for investors who are comfortable taking higher risks and can handle volatility. If you are someone who prefers safety and stability, it’s better to wait, watch, and invest only when you see clear improvement. Sometimes, staying patient is the best investment decision you can make.

Related Posts :

Share This Post