High Growth FMCG Stocks In India 2030: 10 Hidden Gems Investors Are Tracking Right Now

High Growth FMCG Stocks In India 2030: 10 Hidden Gems Investors Are Tracking Right Now | Representative Image

The Indian FMCG sector is quietly entering a powerful growth phase again. If you are searching for high growth FMCG stocks in India 2030, then you are already thinking long term. And honestly, that’s where the real money is made. Most blogs just talk about big names like HUL or ITC, but the actual buzz right now is shifting towards mid and small-cap FMCG companies that can grow faster.

The interesting part is that rural demand is rising faster than urban, quick commerce is booming, and consumers are slowly moving towards branded and premium products. This creates a perfect setup for certain FMCG stocks to outperform by 2030.

Table of Contents

Also Read

Gold Prices Drop Today: 7 Big Reasons Behind The Fall And What Investors Should Watch Next

Key Takeaways On Best FMCG Stocks

- FMCG sector expected to grow aggressively till 2030 with strong rural demand

- Quick commerce is becoming a major growth driver

- Mid and small-cap FMCG stocks are getting more investor attention

- Adani Wilmar and Heritage Foods are among the most searched stocks

- Haldiram IPO can be a big opportunity once listed

- Sugar and agri-based companies can benefit from stable commodity prices

- Brand power and distribution network will decide long-term winners

Why FMCG Stocks Are Trending Again In 2026

Let’s be real. FMCG was kind of slow in the last couple of years. But now things are changing. As per recent data, the sector is expected to grow around 5 to 8 percent in volume in 2026. That may not sound crazy, but for FMCG, that’s actually strong. The bigger story is long term.

| Factor | Impact On FMCG |

|---|---|

| Rural Demand | Faster growth than urban markets |

| Quick Commerce | 75% of e-commerce FMCG sales |

| Inflation | Lower input costs, better margins |

| Market Size | Expected massive expansion by 2030+ |

Also, the market size is already huge and still growing fast. That’s why investors are now hunting for the next big FMCG stock, not just safe ones.

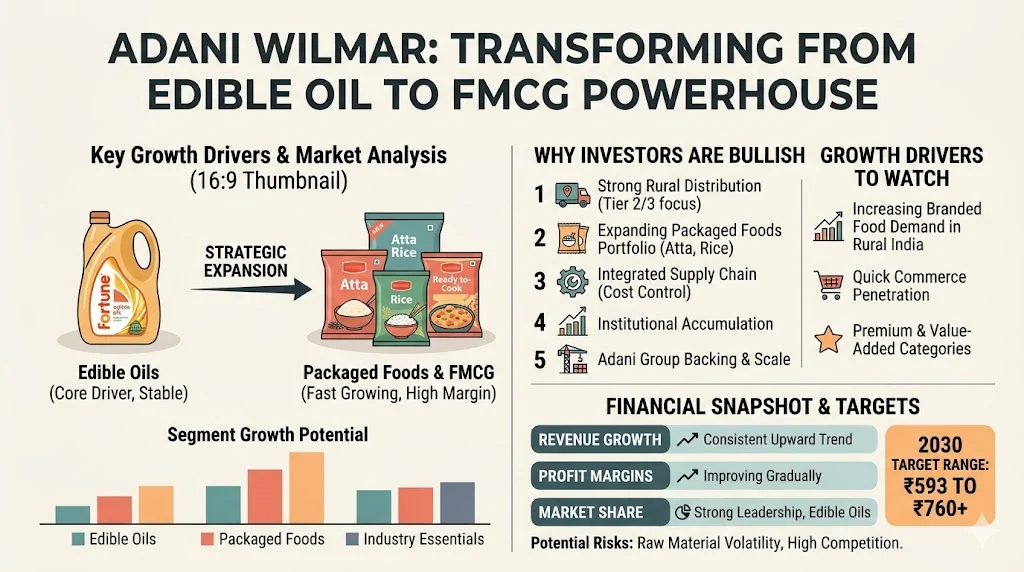

1) Adani Wilmar

This stock is everywhere right now. And for a reason. Adani Wilmar has a strong presence in edible oils with brands like Fortune. It already holds around 19% market share, which is huge. But what makes it more interesting is how the company is slowly transforming from just an edible oil player into a full-fledged FMCG brand.

Key Business Segments

| Segment | Contribution | Growth Potential |

|---|---|---|

| Edible Oils | Core revenue driver | Stable but competitive |

| Packaged Foods | Fast growing | High margin expansion |

| Industry Essentials | B2B segment | Consistent demand |

Why Investors Are Bullish

- Strong rural distribution network reaching deep into Tier 2 and Tier 3 markets

- Expansion into packaged foods like atta, rice, and ready-to-cook products

- Integrated supply chain which helps in cost control and pricing power

- Institutional investors quietly accumulating shares

- Backing of Adani Group providing scale and infrastructure advantage

Growth Drivers To Watch

- Rising demand for branded food products in rural India

- Increasing penetration of quick commerce platforms

- Expansion into premium and value-added food categories

- Better margins due to backward integration

Financial Snapshot (Approx Trends)

| Metric | Trend |

|---|---|

| Revenue Growth | Consistent upward trend |

| Profit Margins | Improving gradually |

| Market Share | Strong leadership in edible oils |

2030 Target Range

₹593 to ₹760+

What Could Go Wrong

- Volatility in raw material prices (especially edible oils)

- High competition from established FMCG giants

- Dependency on commodity cycles

This is not just hype. The business model actually supports long-term growth, especially if the company successfully scales its packaged food segment.

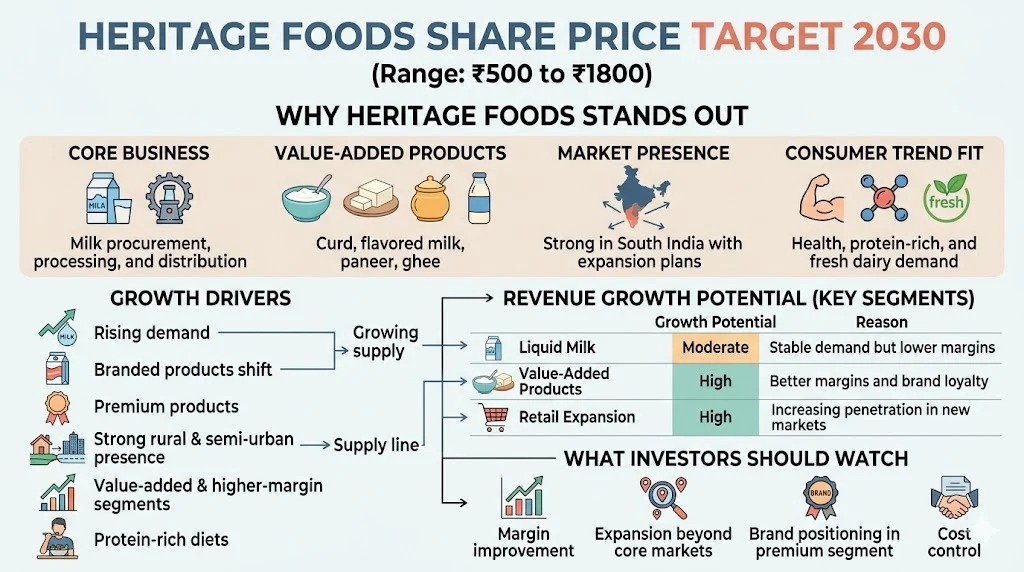

2) Heritage Foods

If you are looking at dairy, this one is interesting. Heritage Foods fits perfectly into the trend of value-added dairy and health-focused consumption. The company is not just a traditional milk supplier anymore; it is gradually transforming into a branded dairy and nutrition-focused business.

Why Heritage Foods Stands Out

| Factor | Details |

|---|---|

| Core Business | Milk procurement, processing, and distribution |

| Value-Added Products | Curd, flavored milk, paneer, ghee |

| Market Presence | Strong in South India with expansion plans |

| Consumer Trend Fit | Health, protein-rich, and fresh dairy demand |

Growth Drivers

- Rising demand for milk and dairy products across urban and rural India

- Increasing shift towards branded and packaged dairy products

- Premium products like flavored milk, curd, and probiotic offerings

- Strong rural and semi-urban presence ensuring steady supply chain

- Expansion into value-added and higher-margin dairy segments

- Growing awareness around protein-rich diets and nutrition

Revenue Growth Potential (Key Segments)

| Segment | Growth Potential | Reason |

|---|---|---|

| Liquid Milk | Moderate | Stable demand but lower margins |

| Value-Added Products | High | Better margins and brand loyalty |

| Retail Expansion | High | Increasing penetration in new markets |

What Investors Should Watch

- Margin improvement from value-added products

- Expansion beyond core regional markets

- Brand positioning in premium dairy segment

- Cost control in milk procurement

2030 Target Range: ₹500 to ₹1800

Yes, the range is wide. That’s because dairy margins can change fast, and profitability depends heavily on input costs and product mix.

3) Haldiram Share Price

Let’s clear one thing. Haldiram is not listed yet. But the buzz is crazy. The company is planning an IPO with a valuation of around $8 to $10 billion. That itself shows the confidence in the brand.

Key IPO Details (Expected)

| Factor | Details |

|---|---|

| Expected Valuation | $8B – $10B |

| Sector | Packaged Foods & Snacks |

| Market Position | Leading Indian snack brand |

| Listing Timeline | Not officially confirmed |

| Investor Interest | Very high (retail + institutional) |

Why this can be huge:

- Strong brand recall across India

- Packaged snacks market is booming

- Expansion in exports and quick commerce

- Huge presence in both traditional retail and modern trade

- Strong product diversification (namkeen, sweets, ready-to-eat)

Growth Drivers To Watch

- Rising Snack Consumption: India’s packaged snack market is growing rapidly due to changing lifestyles and urbanization.

- Global Expansion: Haldiram already has a presence in international markets, and exports can become a major revenue driver.

- Quick Commerce Boost: Platforms like Blinkit, Zepto, and Instamart are increasing impulse snack purchases.

- Premium Product Shift: Consumers are moving towards branded and hygienic packaged food, which benefits established players.

Potential Strengths vs Risks

| Strengths | Risks |

|---|---|

| Strong brand loyalty | High IPO valuation may limit upside initially |

| Wide distribution network | Competition from new-age snack brands |

| Diverse product portfolio | Margin pressure due to raw material costs |

| Export potential | Regulatory and food safety compliance |

What Investors Should Watch After Listing

- Revenue growth consistency

- Expansion into new product categories

- Margin improvement trends

- Market share in organized snack segment

- Performance in quick commerce channels

Once listed, this can become one of the top FMCG stocks in India, especially for investors looking at long-term consumption growth stories.

Mid And Small Cap FMCG Stocks To Watch

This is where things get interesting. These stocks are not talked about much, but they are showing up again and again in search trends.

1) Mishtann Foods Share

Mishtann Foods is one of those under-the-radar FMCG stocks that has started gaining attention due to its focus on staple food products like rice and wheat. While it is still considered a speculative play, the long-term potential depends heavily on execution, branding, and expansion.

Business Overview:

| Segment | Details |

|---|---|

| Core Products | Basmati rice, wheat, pulses |

| Market Focus | Domestic + export markets |

| Industry Type | Agri-based FMCG |

| Growth Stage | Early expansion phase |

Key Growth Drivers:

- Rising demand for packaged and branded staples

- Increasing export opportunities for Indian rice

- Shift from unorganized to organized food sector

- Potential expansion into value-added food products

Strengths:

- Strong presence in staple food category

- Benefiting from consistent agri demand

- Opportunity to scale with better branding

Risks:

- High competition from established brands

- Dependence on raw material prices

- Limited brand recognition compared to leaders

- Financial volatility in past performance

2030 Share Price Outlook (Speculative Range):

| Scenario | Target Range |

|---|---|

| Bear Case | ₹10 – ₹20 |

| Base Case | ₹20 – ₹40 |

| Bull Case | ₹40 – ₹80+ |

Investor Insight:

Mishtann Foods is not a safe bet like large FMCG companies. It is more of a high-risk, high-reward stock. If the company successfully builds a strong brand and improves its financials, it can deliver significant returns by 2030. However, investors should approach it with caution and proper research.

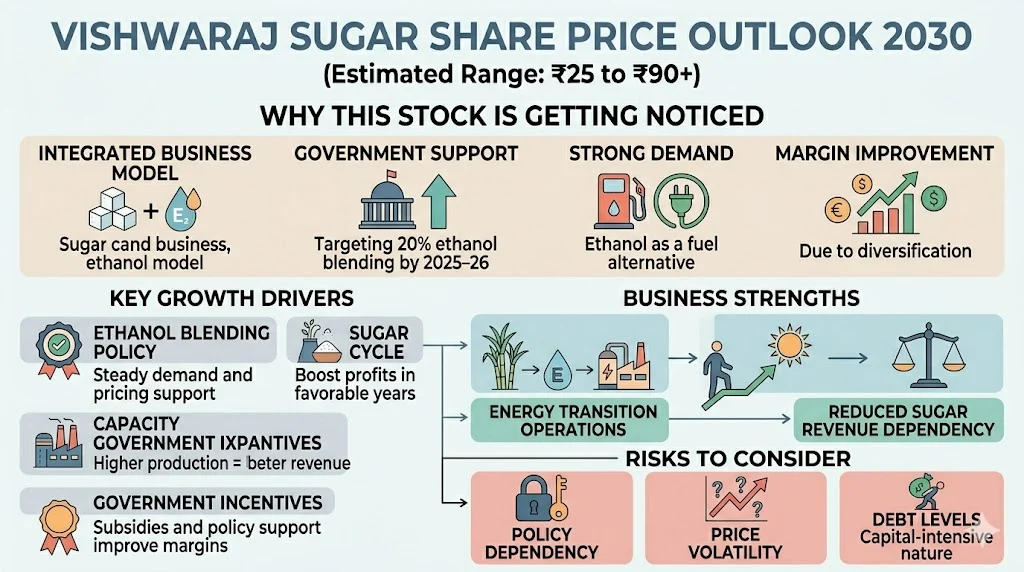

2) Vishwaraj Sugar Share

Vishwaraj Sugar is gaining attention because it sits right at the intersection of the sugar and ethanol story, which is one of the most important long-term themes in India’s agri and energy sectors.

Why this stock is getting noticed:

- Sugar + ethanol integrated business model

- Government support for ethanol blending (targeting 20% blending by 2025–26)

- Strong demand for ethanol as a fuel alternative

- Potential margin improvement due to diversification

Key Growth Drivers

| Factor | Impact |

|---|---|

| Ethanol Blending Policy | Ensures steady demand and pricing support |

| Sugar Cycle | Cyclical but can boost profits in favorable years |

| Capacity Expansion | Higher production = better revenue potential |

| Government Incentives | Subsidies and policy support improve margins |

Business Strengths

- Integrated operations (sugar + ethanol + power)

- Beneficiary of long-term energy transition trends

- Positioned to reduce dependency on pure sugar revenue

Risks to Consider

- High dependency on government policies

- Sugar price volatility

- Debt levels and capital-intensive nature of the business

2030 Share Price Outlook (Estimated Range) ₹25 to ₹90+ depending on ethanol expansion success and sector cycle

This is not a stable FMCG-type stock, but more of a cyclical + policy-driven opportunity. If ethanol demand continues to grow as expected, Vishwaraj Sugar could see strong upside by 2030.

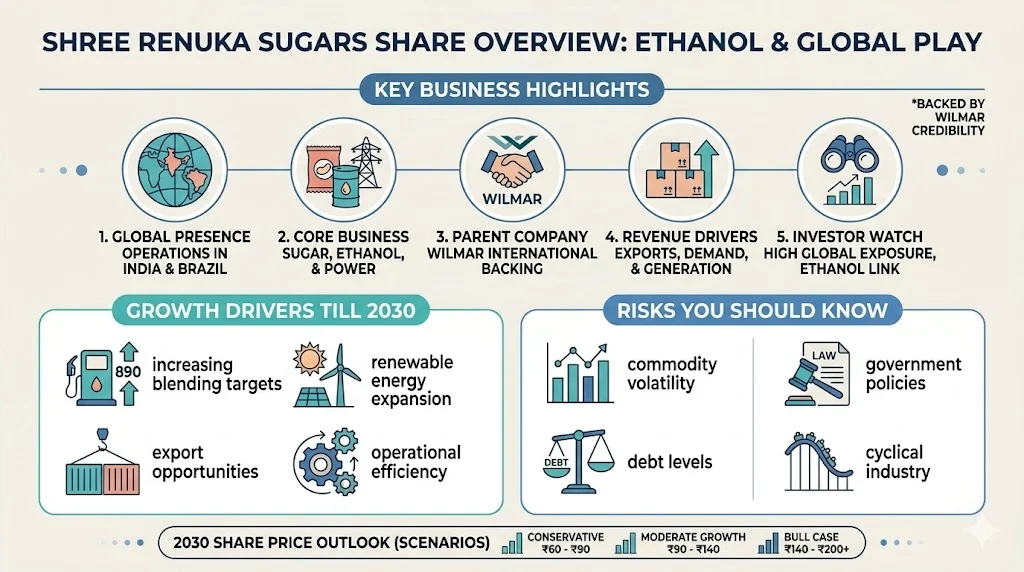

3) Shree Renuka Sugars Share

Shree Renuka Sugars is one of the most talked-about sugar stocks in India, especially because of its global presence and strong linkage with the ethanol blending story.

Key Business Highlights:

| Factor | Details |

|---|---|

| Global Presence | Operations in India and Brazil |

| Core Business | Sugar production, ethanol, and power |

| Parent Company | Wilmar International (strong backing) |

| Revenue Drivers | Sugar exports, ethanol demand, power generation |

Why Investors Are Watching This Stock:

- Strong global exposure gives it an edge over domestic-only players

- Ethanol blending policy in India is a major long-term growth driver

- Backing from Wilmar adds credibility and financial strength

- Potential to benefit from rising sugar prices globally

Growth Drivers Till 2030:

- Increasing ethanol blending targets by the government

- Expansion in renewable energy and power generation

- Export opportunities due to global sugar demand

- Operational efficiency improvements

Risks You Should Know:

- High volatility due to commodity price fluctuations

- Debt levels can impact profitability

- Dependence on government policies

- Cyclical nature of the sugar industry

2030 Share Price Outlook:

| Scenario | Target Range |

|---|---|

| Conservative | ₹60 – ₹90 |

| Moderate Growth | ₹90 – ₹140 |

| Bull Case | ₹140 – ₹200+ |

This stock is not for conservative investors. But if you are okay with volatility and looking for high-risk, high-reward opportunities, Shree Renuka Sugars can be a strong contender in your watchlist for 2030.

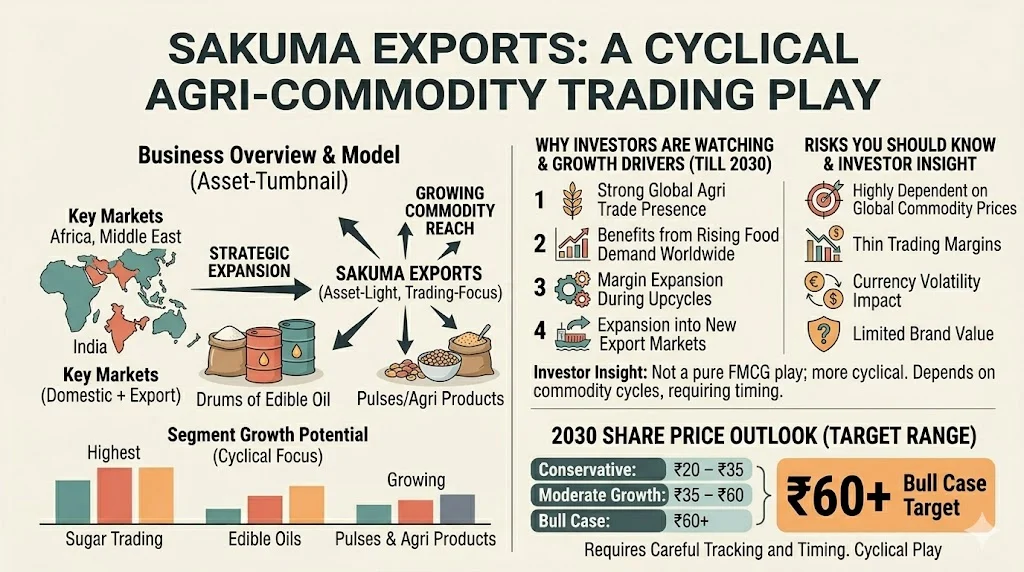

4) Sakuma Exports Share

Business Overview

| Segment | Contribution | Key Markets |

|---|---|---|

| Sugar Trading | High | Africa, Middle East |

| Edible Oils | Moderate | India, Southeast Asia |

| Pulses & Agri Products | Growing | Domestic + Export |

Why Investors Are Watching This Stock

- Strong presence in global agri trade

- Benefits from rising food demand worldwide

- Asset-light business model with trading focus

- Potential margin expansion during commodity upcycles

Growth Drivers Till 2030

- Increasing global demand for food commodities

- Expansion into new export markets

- Favorable government policies for agri exports

- Currency fluctuations that can boost export earnings

Risks You Should Know

- Highly dependent on global commodity prices

- Thin margins compared to branded FMCG companies

- Currency volatility can impact profits

- Limited brand value compared to traditional FMCG players

2030 Share Price Outlook

| Scenario | Target Range |

|---|---|

| Conservative | ₹20 – ₹35 |

| Moderate Growth | ₹35 – ₹60 |

| Bull Case | ₹60+ |

This stock is more of a cyclical play rather than a pure FMCG growth story. If global demand remains strong and commodity cycles stay favorable, Sakuma Exports can deliver decent returns. However, it requires careful tracking and timing.

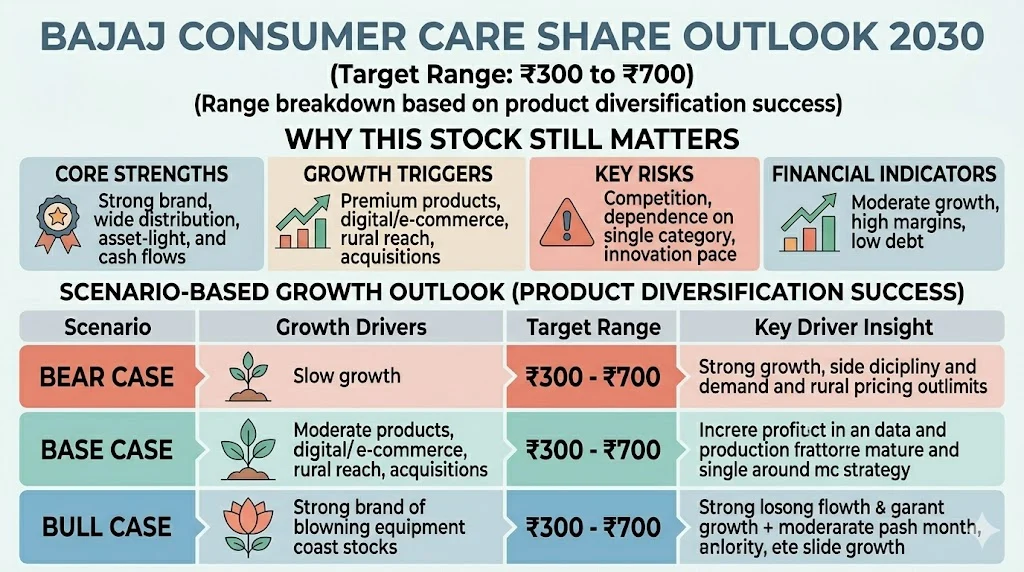

5) Bajaj Consumer Care Share

Bajaj Consumer Care is a well-known name in the personal care segment, especially for its flagship brand Bajaj Almond Drops Hair Oil. The company is now trying to reposition itself beyond just hair oil and tap into the broader wellness and grooming market.

Core Business Strengths:

- Strong brand recall in hair care category

- Wide distribution network across urban and rural India

- Asset-light business model with consistent cash flows

Growth Drivers:

- Expansion into premium and value-added personal care products

- Increasing demand for grooming and wellness products among younger consumers

- Focus on digital marketing and e-commerce channels

- Potential product diversification beyond hair oils

Key Financial Indicators (Snapshot):

| Metric | Insight |

|---|---|

| Revenue Growth | Moderate but stable |

| Profit Margins | Healthy due to strong brand pricing |

| Debt Level | Low, financially stable |

| Market Position | Strong in hair oil segment |

Opportunities vs Risks:

| Opportunities | Risks |

|---|---|

| Premium product expansion | High competition from new-age brands |

| Growth in rural consumption | Dependence on single product category |

| E-commerce and D2C growth | Slow innovation compared to peers |

2030 Share Price Target Range: ₹300 to ₹700

To understand this range better, let’s break down the possible scenarios:

| Scenario | Expected Growth Drivers | Target Range |

|---|---|---|

| Bear Case | Slow demand growth, limited product expansion | ₹300 – ₹400 |

| Base Case | Stable sales growth, moderate brand expansion | ₹400 – ₹550 |

| Bull Case | Strong diversification, premium product success | ₹550 – ₹700 |

Why This Stock Still Matters

This stock may not be a hyper-growth story, but it offers steady growth potential with strong brand backing. It fits well for investors who prefer consistency over aggressive risk.

Key Strengths

- Established brand presence in its category

- Consistent demand due to daily-use products

- Strong distribution network across urban and rural markets

- Ability to maintain stable margins even during market fluctuations

Growth Triggers To Watch

- Expansion into premium or value-added product segments

- Increased focus on digital and quick commerce channels

- Rural market penetration and deeper distribution reach

- Strategic partnerships or acquisitions

Risks To Consider

- Intense competition from both large FMCG players and new startups

- Limited innovation compared to high-growth peers

- Dependence on a few core product categories

Investor Perspective

If the company successfully diversifies its product portfolio and adapts to changing consumer trends, it can become a solid long-term FMCG play. It may not deliver explosive returns, but it can provide stable and predictable growth over time, which is equally valuable in a balanced portfolio.

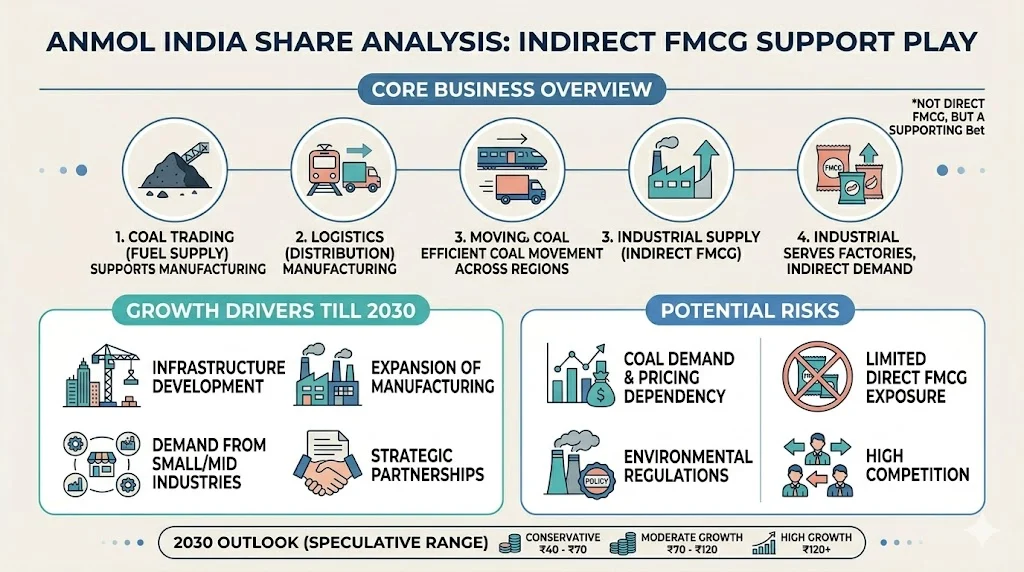

6) Anmol India Share

Anmol India is not a direct FMCG company, but it plays an important supporting role in the ecosystem. The company is primarily involved in coal trading, which is a key input for many manufacturing industries, including FMCG production units.

Because of this indirect linkage, its growth can align with overall industrial and consumption demand in India.

Core Business Overview:

| Segment | Role in Economy | FMCG Connection |

|---|---|---|

| Coal Trading | Supplies fuel to industries | Supports manufacturing operations |

| Logistics | Distribution of coal across regions | Improves supply chain efficiency |

| Industrial Supply | Serves multiple sectors | Indirect demand from FMCG factories |

Why Investors Are Watching This Stock:

- Rising industrial activity in India

- Increasing demand for energy and raw materials

- Expansion into new supply chains

- Potential to benefit from overall economic growth

Growth Drivers Till 2030:

- Infrastructure development boosting energy demand

- Expansion of manufacturing sector

- Strong demand from small and mid-scale industries

- Strategic partnerships and supply contracts

Potential Risks:

- Dependency on coal demand and pricing

- Environmental regulations and policy changes

- Limited direct FMCG exposure

- High competition in commodity trading

2030 Outlook (Speculative Range):

| Scenario | Target Range |

|---|---|

| Conservative | ₹40 – ₹70 |

| Moderate Growth | ₹70 – ₹120 |

| High Growth | ₹120+ |

This is not a typical FMCG stock, so it should be treated differently in your portfolio. It can act as a supporting growth play rather than a core FMCG investment. These are not “safe” stocks. But yes, they are high growth bets if things go right.

What Public Is Saying (Twitter/X Insights)

This is where you get the real pulse. People are not just talking about big FMCG companies anymore. The focus is shifting.

Common themes from public opinion:

- Rural India is the real growth engine

- Quick commerce is changing buying behavior

- Investors prefer companies with strong distribution

- Brand loyalty still matters a lot

- Premium products are gaining traction

One interesting thing people are pointing out is how companies like Adani Wilmar are scaling because of supply chain control and pricing power. Also, there is strong belief that FMCG will remain a “safe growth” sector till 2030.

What Most Articles Miss (Important Insights)

After going through multiple articles, one thing is clear. Most of them only focus on large cap stocks. But they miss these key points:

- Small cap FMCG stocks can give higher returns

- Quick commerce impact is underestimated

- Rural consumption is more important than urban now

- Brand + distribution combo is the real moat

- IPO opportunities like Haldiram can be game changers

If you ignore these, you are basically missing the full picture.

Risks You Should Not Ignore

Let’s not get over excited. Every sector has risks.

- Raw material price fluctuations

- High competition from new brands

- Regulatory changes

- Rural demand dependency

- Overvaluation in some stocks

So yeah, don’t blindly chase hype.

Final Thoughts

If you are looking for high growth FMCG stocks in India for 2030, this is honestly a great time to start paying attention and building your watchlist.

The sector is changing faster than most people realize. It’s no longer just about “safe” companies. New trends like rural demand, quick commerce, and premium products are quietly reshaping the entire space.

From my perspective, the real winners won’t just be the biggest names. They’ll be the companies that can adapt, build strong brands, and stay efficient as they grow. That’s what you should keep an eye on. And one small piece of personal advice don’t rush. Take your time, understand the business, and invest only when you feel confident. This article is just a starting point to help you explore, not a final answer.

Related Posts :

Share This Post